Economic modelling and analysis by Treasury explores 3 scenarios of Australia’s transition to net zero by 2050 (Treasury, 2025). This work informed the Australian Government’s Net Zero Plan and Sector Plans and includes potential economy‑wide and sector‑specific emissions reductions pathways. Treasury modelling provides useful insights on the potential cost‑effective timing, sequencing and size of sectoral contributions to the economy‑wide emissions reduction task. The Treasury modelling and analysis serves as part of the evidence base for potential decarbonisation pathways for the Industrial sector.

In this section, we refer to the Baseline Scenario, in which Australia efficiently builds on existing climate policies and trends to achieve its net zero targets. The Treasury’s Baseline Scenario illustrates a cost-effective pathway for the industrial sector to contribute to reaching Australia’s net zero goal.

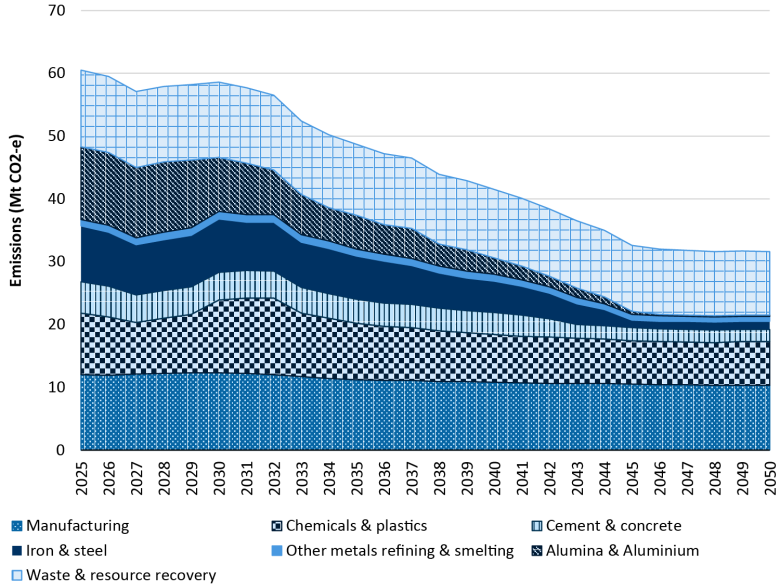

Treasury’s Baseline Scenario projects that emissions from Australia’s industrial and waste sector will reduce from 61 Mt CO2‑e in 2025 to 32 Mt CO2‑e in 2050. Investments in abatement technologies are expected to be a significant driver for this emissions reduction. These technologies include electrification and adoption of less emissions‑intensive production processes, which are projected to reduce emissions intensities across the sector by 72% by 2050. Emissions from waste remain a small but persistent source of emissions. Abatement through methods such as landfill gas capture is expected to reduce emissions in the sector by 2.5 Mt CO2‑e by 2050.

This modelling projects that Australia will be able to maintain (and in some cases, expand) its existing industrial capabilities. However, the decarbonisation of Australian industries will not be straight forward. Navigating a pathway to net zero will need careful coordination and planning between governments and the private sector. Treasury’s Baseline Scenario presents a case where we have successfully achieved this transformation.