These 9 subsectors represent 120,000 Australian businesses that generated $205.8 billion in gross value added (GVA), the equivalent of 7.7% of GDP, in 2023–24. Australia’s industrial sector provides over one million jobs, which is approximately 8% of Australia’s total employment.

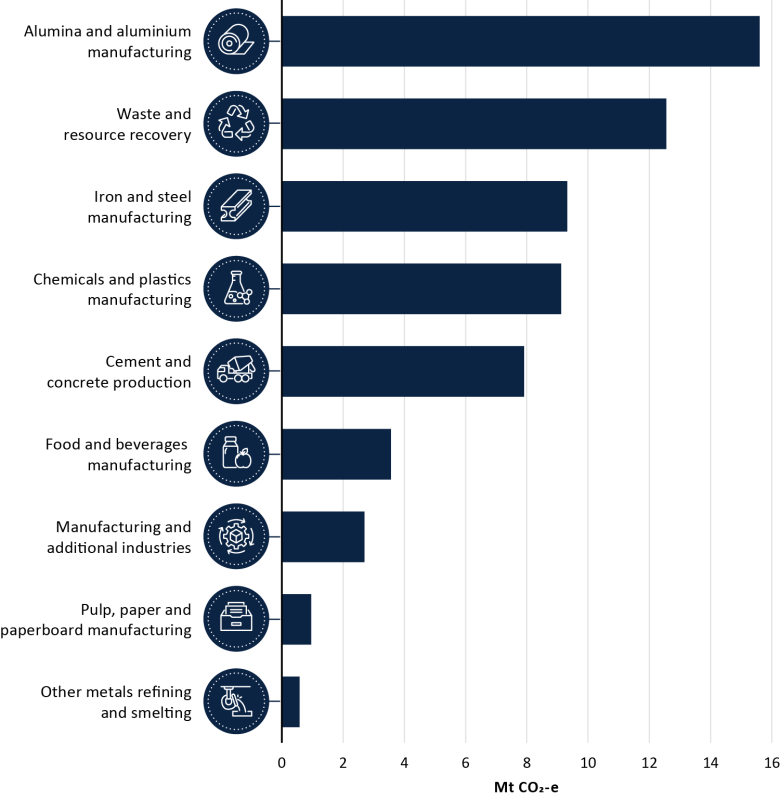

Australia’s industrial sector represents 14% of the economy’s scope 1 emissions (DCCEEW, 2025a). Of the 9 industrial subsectors, 5 represent almost 90% of industrial scope 1 emissions:

- alumina and aluminium

- waste and resources recovery

- iron and steel

- chemicals and plastics

- cement and concrete production.

Industrial facilities, particularly alumina and aluminium, steelworks and datacentres, are also large electricity and energy users.

Key activities that contribute to scope 1 emissions from industry include:

- Process heating emissions from the combustion of gas, coal and oil to create heat and energy for industrial activities. For example, alumina, steel and food and beverage manufacturing burn these fuels to generate heat for calciners, furnaces and boilers.

- Industrial processes that produce greenhouse gases because of the feedstock and reactions needed for their production. Traditional cement, iron and ammonia production rely on chemical reactions that produce greenhouse gases.

- Decomposing organic materials producing methane emissions that can escape into the atmosphere, such as from sewage, landfill and industrial wastewater.

The Australian Government has committed over $22.7 billion towards a Future Made in Australia. This agenda aims to maximise the economic and industrial benefits of the global net zero transition and secure Australia’s position in the global landscape. The Industry Sector Plan is part of this effort.

We developed this plan through targeted engagement. We heard how many Australian industrial businesses, including large and export‑focused businesses and forward‑looking small and medium‑sized businesses, are already taking steps towards net zero. This plan also uses findings from concurrent consultation processes including the Climate Change Authority 2024 Sector Pathways Review and the DISR Green Metals Consultation Paper.

In the immediate term, Australian industry is facing multiple significant challenges transitioning to net zero. These include global market disruptions driving volatile energy prices, limited opportunities to electrify in some sectors, aging infrastructure and intensifying competition in global markets. Sectors such as smelting, cement, glass, and ammonia production are particularly challenging to decarbonise. As Australia pursues the Future Made in Australia agenda and seeks to grow its manufacturing base, we must address these transitional pressures. This will ensure our long‑term energy security, industrial competitiveness and economic resilience.

The most critical challenges are to efficiently deliver and use gas and electricity as industries move towards net zero, accelerate the rollout of renewable electricity and fill technology gaps for certain high heat industrial processes. Maintaining industrial competitiveness and capabilities during the transition period is equally important to set us up to achieve our net zero and Future Made in Australia ambitions. Alongside this plan, the Net Zero Plan and the Electricity and Energy Sector Plan explore these challenges and how industry and governments are addressing them.

Achieving the industrial net zero transition will be complex. It will need careful regional planning, a skills ready workforce and reliable and affordable access to renewable energy. It will also need significant capital investment. But decarbonising Australia’s industrial sector presents opportunities that will benefit communities and the broader economy. The Industry Sector Plan sets out a way for community, government and industry to work together to achieve these opportunities: to reduce emissions, develop new export opportunities and promote economic growth.

The Net Zero Industry Sector Plan sets out a pathway around 3 principles: