Emission trends to date, and the projections on status quo

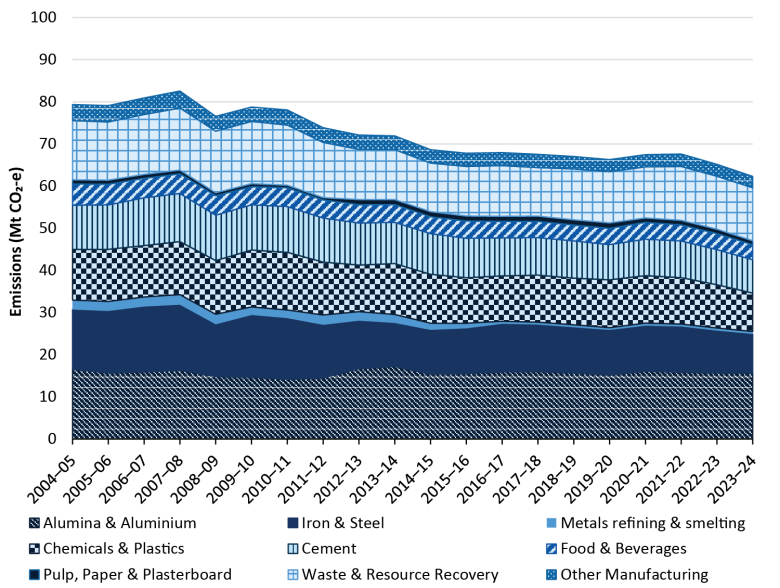

Since 2005, the industrial subsectors direct emissions have decreased slightly, see below. Some of the declines can be attributed to the global financial crisis, particularly in the immediate years following 2007 (House of Representatives, 2009). Other declines in emissions are likely a result of improvements in efficiency as well as the closure of industrial facilities over this period.

Emissions have otherwise remained mostly flat, reflecting a stable period of industrial activity. More recent disruptions triggered by the invasion of Ukraine and the accompanying gas price increases are partly responsible for the decreases in emissions in the years 2022 to 2024.