Australia is a resource-rich country. The global drive towards net zero requires the production of critical minerals and metals for renewable energy and new clean and advanced technologies, and as an economy we stand to benefit.

The Resources Sector Plan outlines a pathway for Australia to continue thriving as a global exporter of resources commodities, underpinned by a set of enduring comparative advantages that support ongoing prosperity.

The nation’s rich endowment of minerals and resources provides a strong foundation for production of and innovation in low emissions and clean energy embedded products. Our low sovereign risk and stable political environment have fostered sustained investment confidence. Coupled with secure trade routes and our strategic proximity to fast-growing Indo-Pacific markets, Australia maintains a well-earned reputation as a reliable and trusted exporter of energy and resources.

This plan gives an overview of the sector, emissions profile and credible abatement pathways, anchored by the Safeguard Mechanism.

To fully realise the economic and strategic potential of its natural resources, Australia must build sovereign capability in decarbonised minerals extraction and processing, as market demand for low emissions and clean energy embedded products continues to rise.

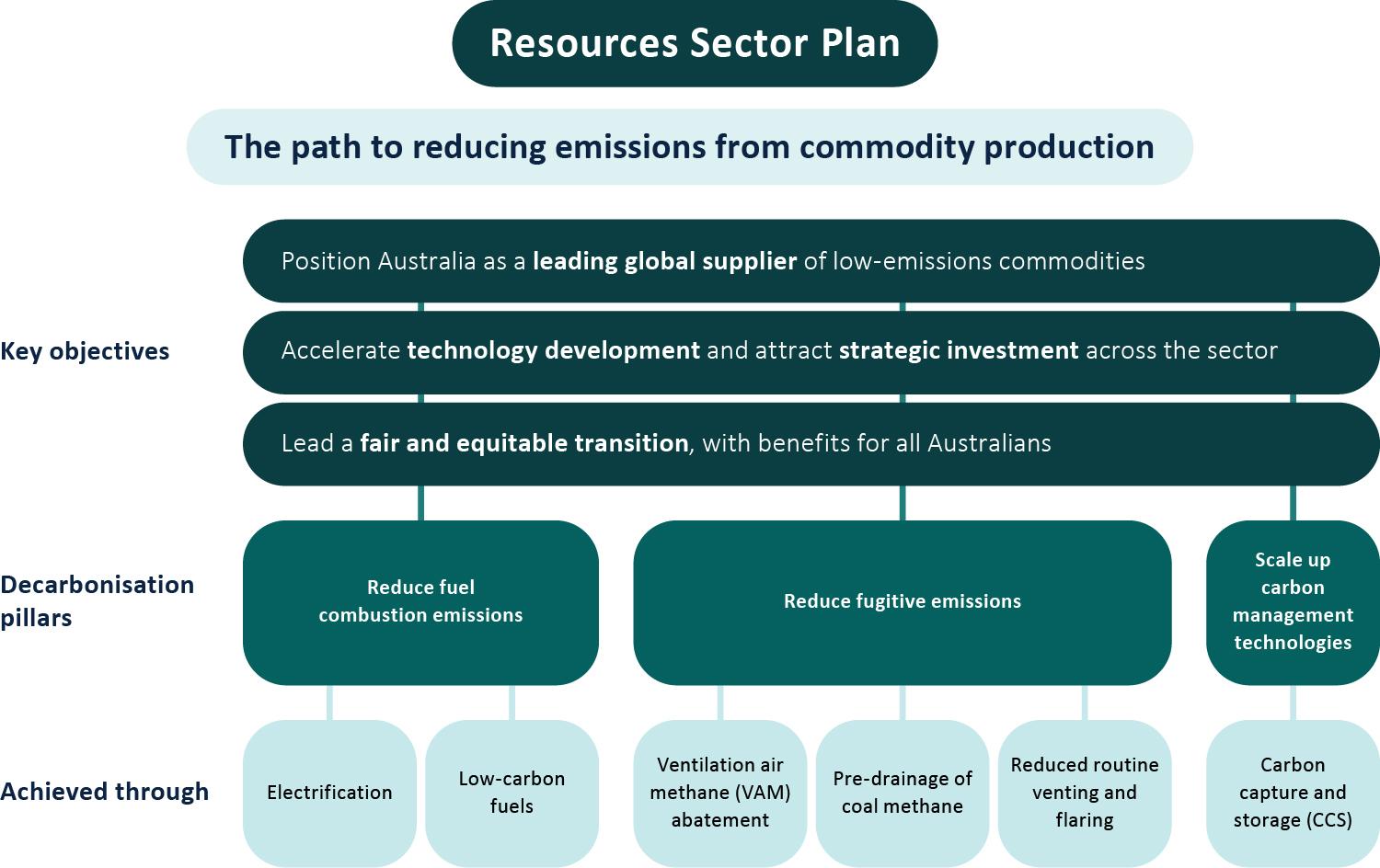

The Future Made in Australia agenda will support this new capability to strengthen global supply chains and position Australia as a reliable, value-adding export partner in low emissions commodities. New trade in critical minerals will complement existing trade in energy commodities, to ensure energy security for both domestic and international markets.

The government recognises that emissions reduction efforts are changing the way the resources sector operates. Emissions reduction in Australia’s resources sector will be shaped by a mixture of evolving global commodity demand, the adoption of low emissions technology and breakthroughs in technological innovation. The Safeguard Mechanism covers 87% of the resources sector’s emissions and 64% of the facilities covered by the SGM are resources operations. This places most of the sector’s emissions on a predictable trajectory to net zero by 2050 and encourages emissions reductions, achievable through electrification, methane abatement and switching to low-carbon fuels where available.

Net zero scenarios, including those set out in Treasury’s modelling report, project a decline in gas trade due to a global shift to clean energy. However, gas will remain critical for energy security and it is an important transition fuel to reach net zero. The role of gas will change over time, with some sectors electrifying. Other areas of our economy and those of our trading partners, like large industrial users, power generation, and electricity firming and peaking support will still require gas over the medium to long-term. We anticipate gas use to support a growing minerals processing industry and to achieve emissions reductions amongst industrial coal users until renewable energy alternatives, like hydrogen or biomethane, are commercially available at scale. Government policy is encouraging a reduction in emissions from gas production and use, while the government’s Future Made in Australia investments will help to make low-carbon alternatives like hydrogen competitive.

New technology developments and carbon management solutions will also be critical to achieve net zero. Many companies are leading the way by trialling equipment that reduces diesel consumption, minimising venting and flaring, developing their own new carbon capture technology, investing in multi-billion-dollar carbon capture and storage projects, looking at opportunities to adopt circular economy principles or investing in expanded renewable energy generation. Methane abatement technologies are an important focus for coal and gas extraction industries, with ventilation air methane abatement technology particularly important for underground coal mines, along with technology enhancements in the detection and measurement of methane emissions.

The resources sector is working on lowering its emissions intensity because demand is growing for lower emissions commodities and having a credible pathway to net zero is key to the sector’s social licence. Communities affected by the transition must be supported to participate in the net zero economy. This will require inclusive planning and decision-making processes that reflect community needs, with potential to share in the benefits.

The Resources Sector Plan includes insights from consultation with a wide range of stakeholders, identifies opportunities for technology development and highlights cross-cutting considerations that must be taken into account when developing new policies. Together, the 6 sector plans and Australia’s overarching Net Zero Plan harness the nation’s comparative advantages to unlock the economic opportunities of the transition to net zero.