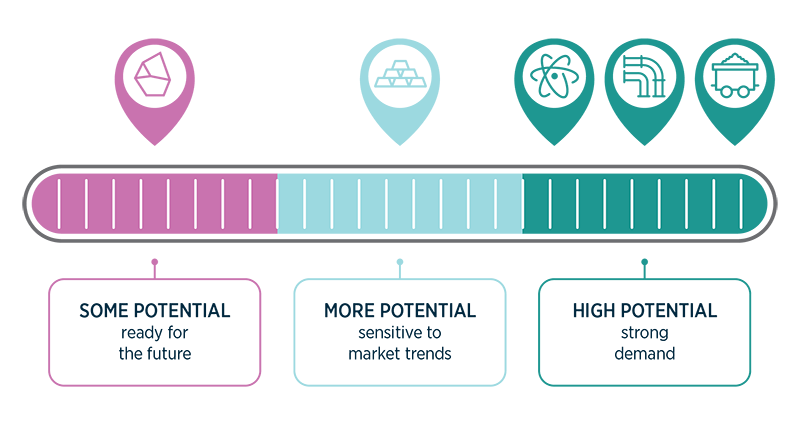

The North Bowen and Galilee are best known for their high quality coal. However, there has been widespread exploration for other resources in the basins. Industry has developed some of these resources, and there may be significant value in investing in further operations (figure 1).

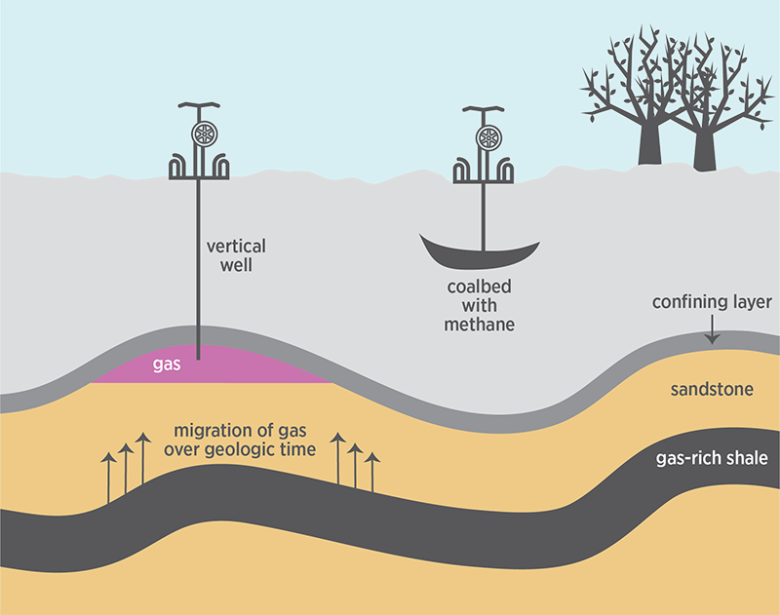

Gas fields are abundant within the basins. A small number of active players have explored the basins extensively. Industry has uncovered significant quantities of gas trapped within coal seams and deeper sandstone. If all the gas estimated to reside in the North Bowen and Galilee was sold today, it would be worth over $100 billion. Current production is limited and explorers are seeking to prove resource economics in their license areas.

Metallurgical and thermal coal have widespread reserves and resources. There is significant coal production in the basins today, including over 60% of Australia’s total metallurgical coal production. Additional investments are in various stages of project development.

Gold sees modest production within the basins, accounting for only 5% of Australia’s total gold production. A planned expansion to a project at Ravenswood will significantly scale-up production. There are several undeveloped gold deposits in the North Bowen and Galilee region. Almost all are at early stages of feasibility assessment.

Critical minerals, such as vanadium, are present in significant quantities, but are not being produced. Reserves and resources are modest compared to the other commodities in the North Bowen and Galilee. Comparatively, there are more extensive critical mineral deposits and projects being developed elsewhere across Australia.

Hydrogen projects in the areas surrounding the basins are in the early development stage. There is significant momentum towards developing these projects, from both industry and the government. However, industrial pathways for clean hydrogen are still emerging.