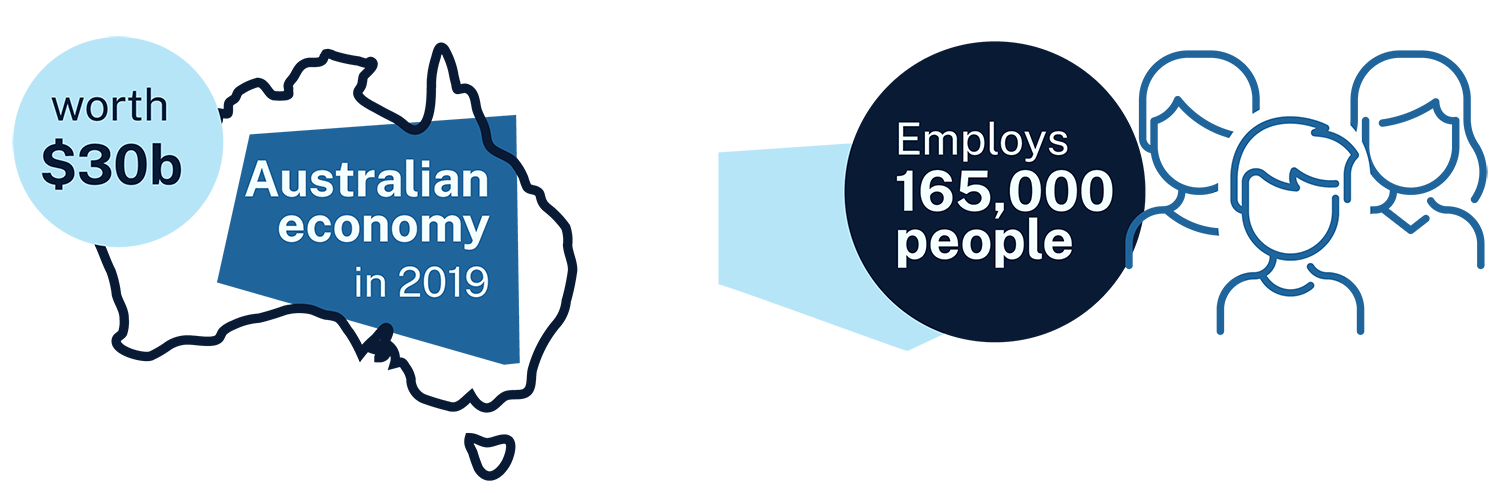

In 2019, the Australian rail industry contributed around $30 billion (1.5%) to the national economy and employed over 165,000 full-time equivalent people (ARA 2020) in ‘above and below’ rail design, manufacturing, construction, maintenance, and operations.

Rolling stock manufacturing is a small but important part of the story. On average, the sector directly employs around 5,900 people and has contributed $875 million in industry value added (IVA) every year over the last decade to June 2023. However, Australia remains a net importer of rolling stock and components. While exports averaged $50 million over the last decade, the average value of imports was over $1.1 billion over the same period (IBISWorld 2023).

Australia’s rail manufacturing sector has previously played a more substantial role in the provision of government owned rolling stock, supporting thousands of high-quality enduring jobs and creating economic value in our communities. With the support of state and territory governments and other stakeholders, Australia can grow a more globally competitive rail manufacturing sector that lifts productivity, improves social and environmental outcomes, and creates economic value. The Australian rail manufacturing sector faces well understood challenges. Change to address these challenges will require commitment and a strong spirit of collaboration across jurisdictions. And there are national and global factors that strengthen the case for reform.

Rail interoperability is a priority for National Cabinet and has been a major focus for the Infrastructure and Transport Ministers Meetings (ITMM) over recent years. While the interoperability agenda has a focus on rail safety outcomes, it also has a productivity focus which can be addressed in part through national cooperation on rail procurement and manufacturing.

State and territory governments are set to make significant investments in rolling stock. An assessment of publicly available rolling stock procurement pipelines suggests this investment will be around $19 billion between 2023 and 2032. This includes around 500 new passenger train and light rail vehicles across 13 known current procurements in 6 states and 2 territories. Almost two-thirds (65%) of this new rolling stock are expected to be manufactured and assembled in Australia and there is opportunity to improve outcomes through national cooperation.

Projected population growth in major urban and regional centres will continue to drive demand and subsequent investment in passenger and freight rail. In addition, much of Australia’s current rail infrastructure and rolling stock is ageing and will require asset renewal over time.