Latest developments

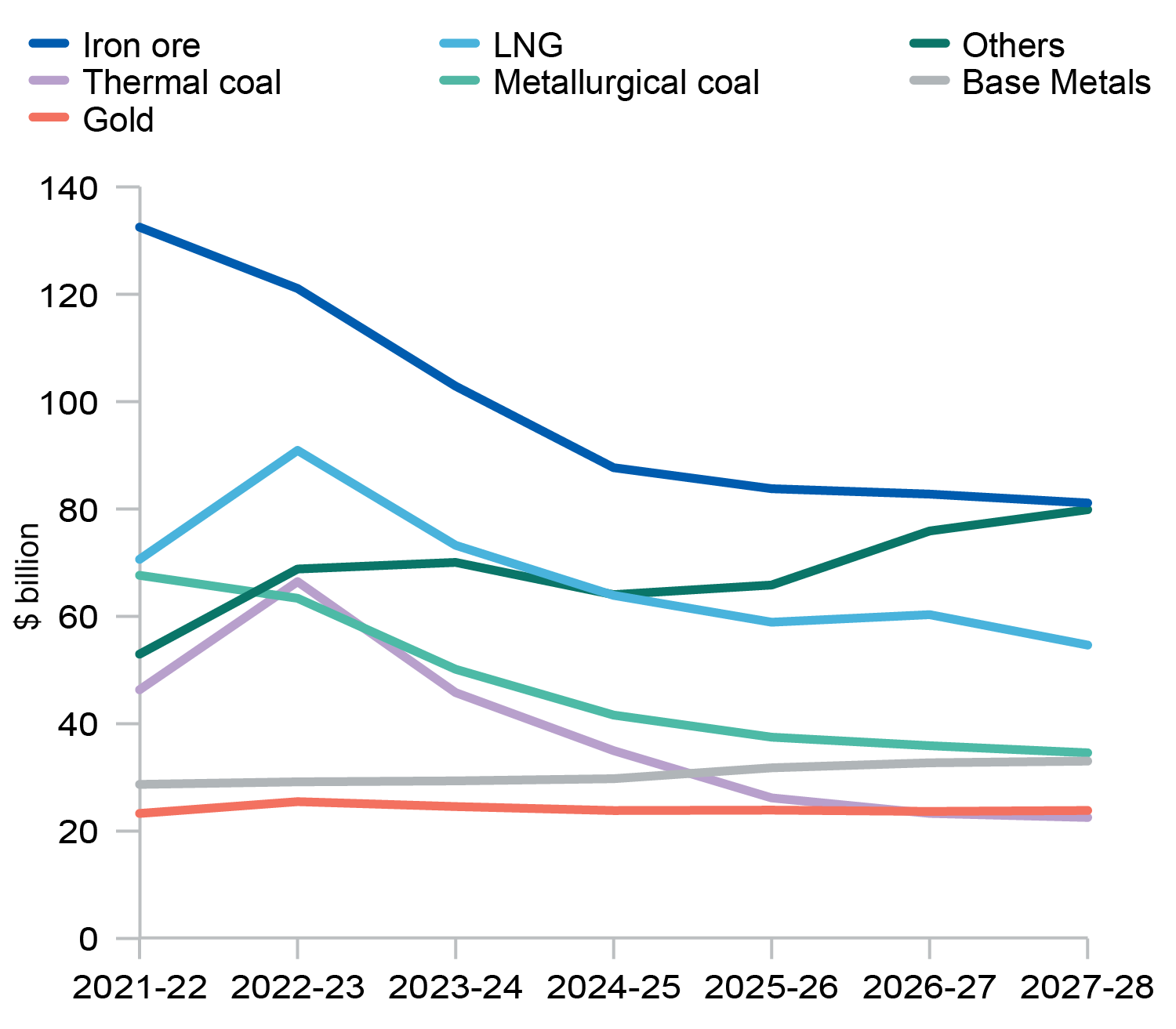

Australia’s resource and energy export earnings are forecast to reach a new record of $464 billion in 2022–23.

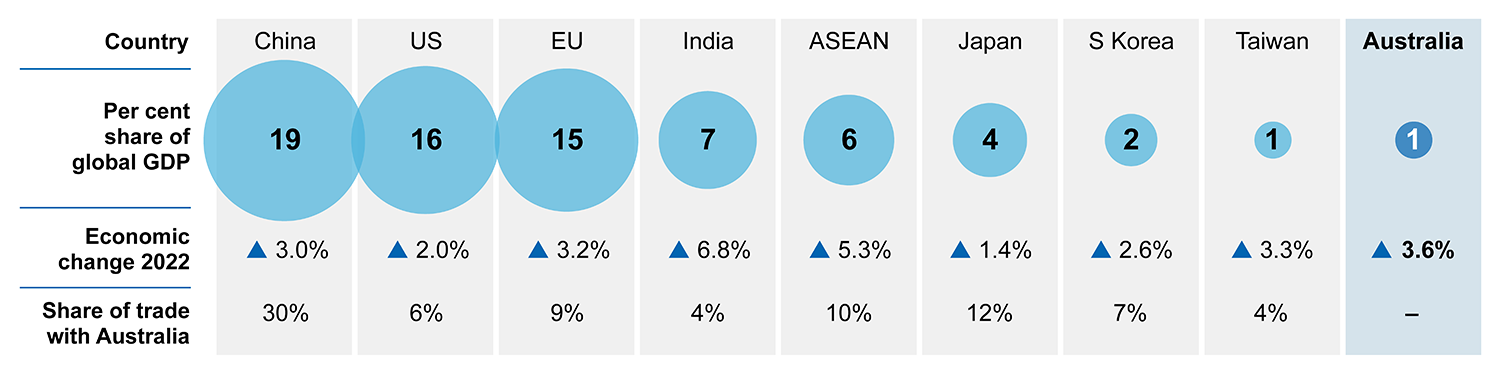

- Energy commodity prices continue to unwind the war-driven spike of 2022 as markets reorganise. But with China ending its COVID lockdowns, commodity prices should level out in 2023.

- High energy commodity prices and strength in the US dollar are driving a surge in export earnings. After a record $422 billion in 2021–22, resource and energy export earnings are forecast to lift to $464 billion in 2022–23, before falling back over the outlook period.

- By 2028, the export value of lithium and base metals (and their component inputs) will equal the export value of all coal types.