Latest developments

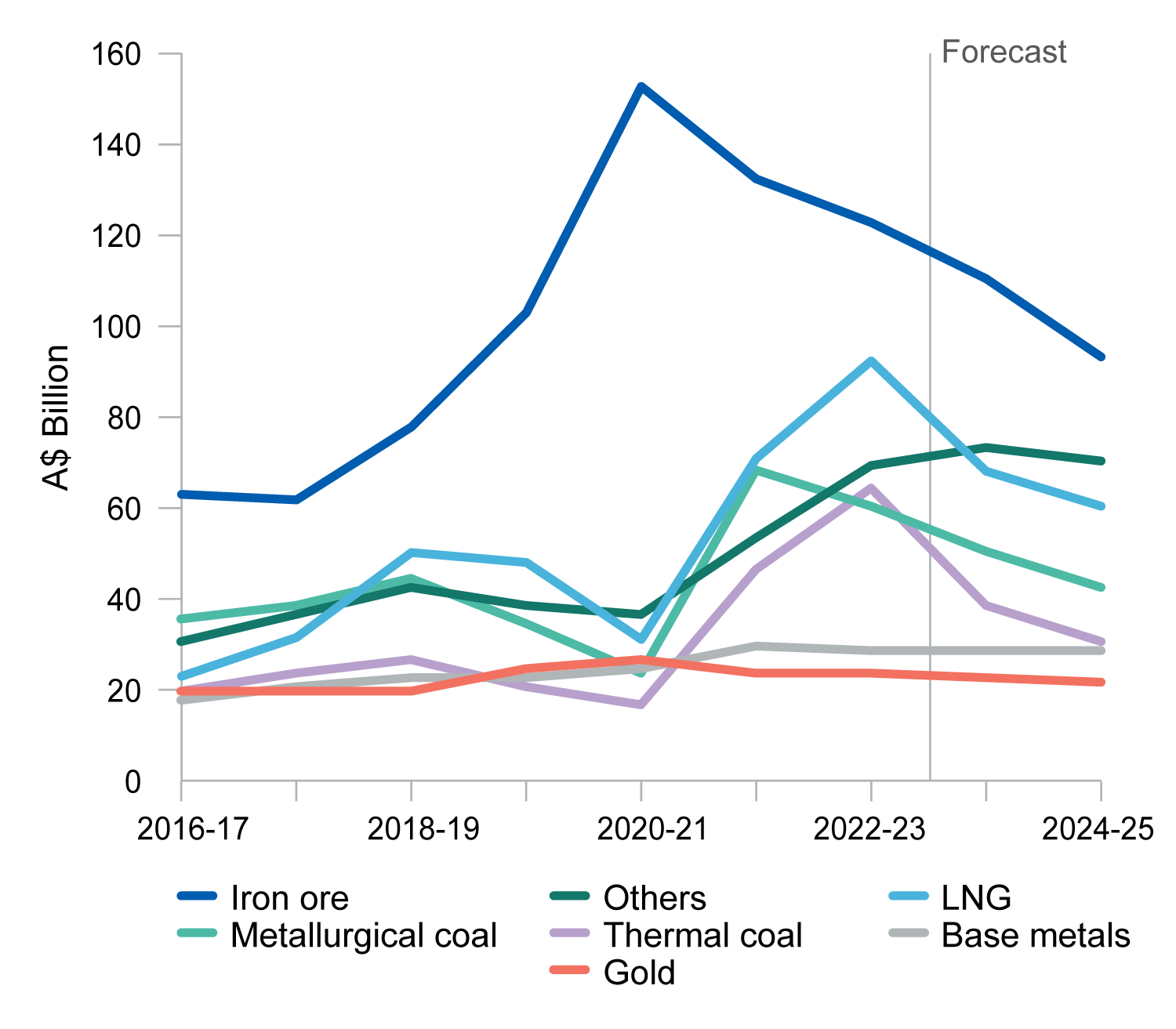

Australia’s resource and energy export earnings are forecast to decline to $390 billion in 2023–24 from a record of $460 billion in 2022–23.

- Resource and energy commodity prices continued to fall in the June quarter of 2023, as world economic growth slowed further under the impact of tighter monetary conditions policy in some major economies.

- Lower energy prices will drive a sharp decline in resource and energy export earnings in 2023–24 to $390 billion, with another fall likely in 2024–25. Lower prices reflect weaker-than-expected world demand and improving world commodity supply. Supply is rising as a result of the end of La Nina climate conditions in the Southern Hemisphere, and as trade is reorganised as a result of sanctions imposed on Russia for its invasion of Ukraine.

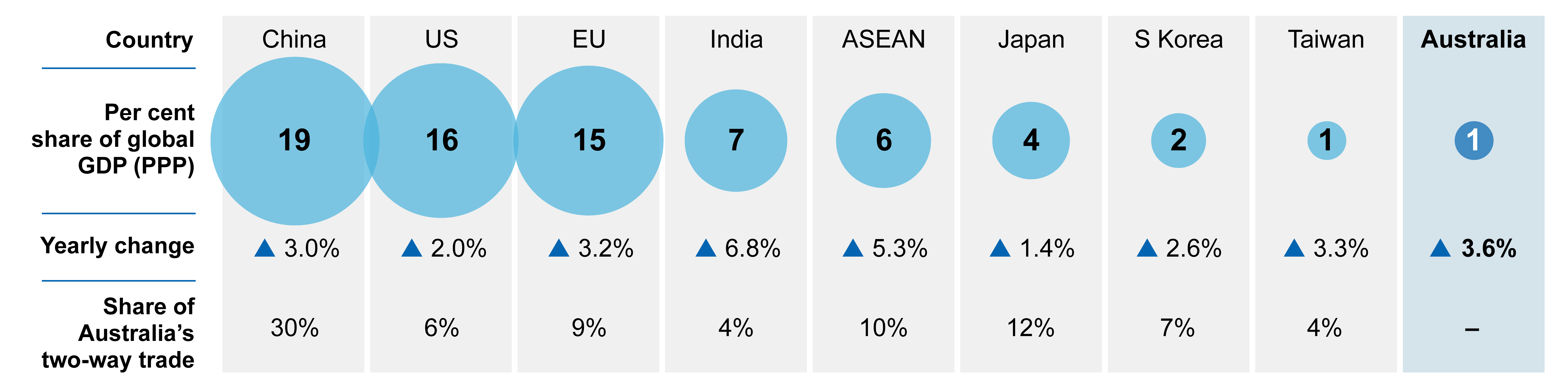

- The incentives for developing low emission technologies under the US Inflation Reduction Act have sparked an increase in global investment in the resource and energy sectors. Australia is well placed to benefit from the Act.