Since the December 2025 Resources and energy quarterly (REQ), forecasts for Australia’s resource and energy commodity exports in 2025–26 and 2026–27 have been revised up sharply. Driving the upgrade has been higher-than-expected prices for energy commodities – due to supply disruptions in the Middle East – and ongoing strong gold prices. Export earnings are expected to fall modestly by 2030–31 as earlier upward revisions in 2025–26 and 2026–27 unwind.

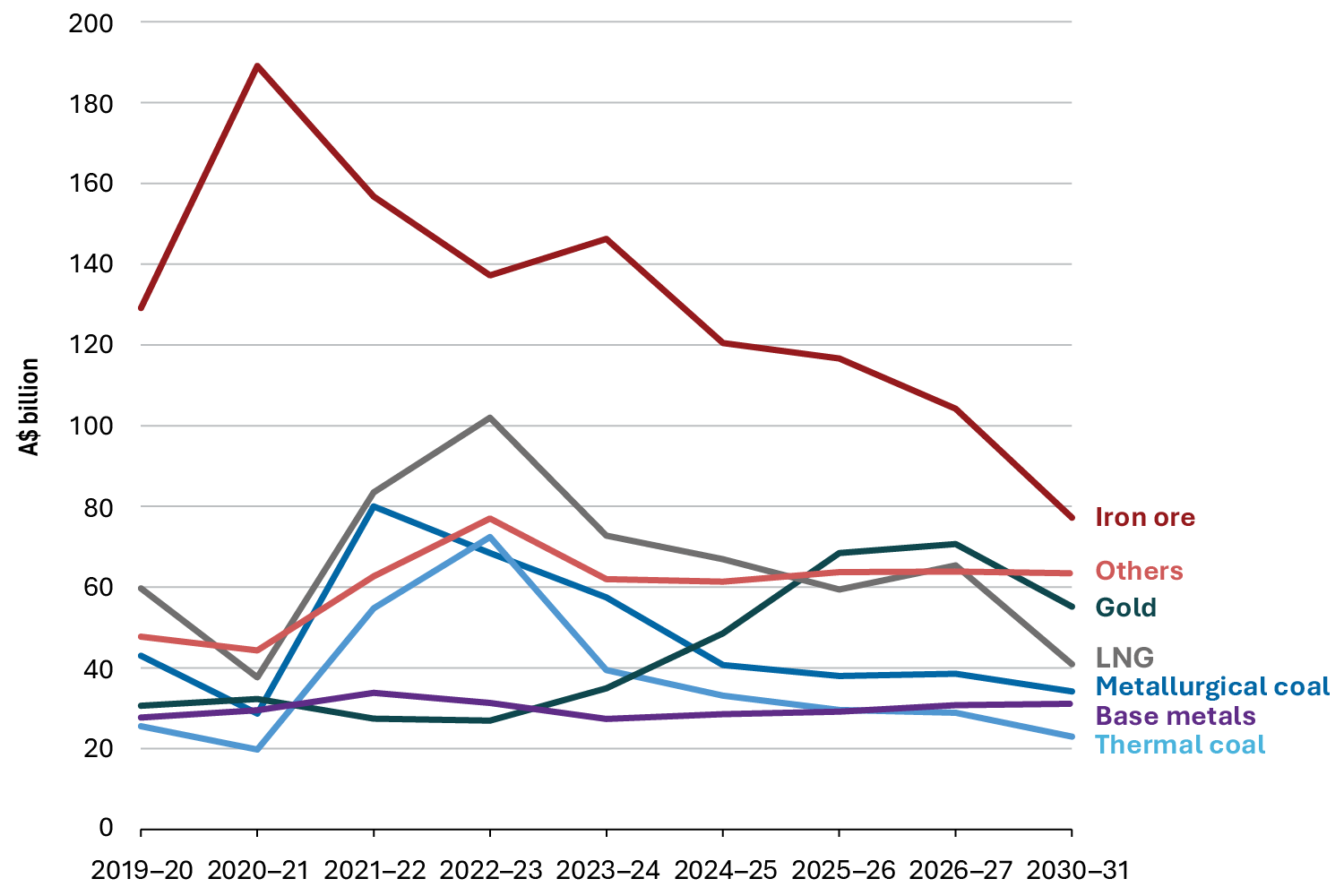

- The outlook for Australia’s exports of resource and energy commodities is stronger than at the time of the December 2025 REQ report. Resource and energy exports are now estimated to have risen to around $405 billion in 2025–26 from $385 billion in 2024–25 and are forecast at $416 billion in 2026–27. Exports are forecast to fall to $371 billion ($325 billion in real terms) in 2030–31.

- World economic growth is expected to be 3.1–3.2% over the 5-year outlook period, similar to pre-pandemic growth rates. The Strait of Hormuz blockade and shifting trade barriers will detract from world growth in the short term, while easier fiscal policy and strong investment will support activity. Investment will be driven by rising artificial intelligence (AI) usage and data centre investment, efforts to boost supply chain security and the global energy transition.

- Within the resource and energy commodity exports, gold exports are forecast to peak at $73 billion in 2026–27. But iron ore will remain our biggest export over the outlook period. Our low production costs and proximity to the fast-growing Asian region will help Australia compete against rising Brazilian and Guinean iron ore output.

This publication assumes a near term resolution of disruptions in the Middle East as the central scenario.

An alternative scenario, where trade disruptions continue for several more months, leads to longer and higher prices for energy commodities. In the alternative scenario, the longer period of elevated prices leads to stronger export earnings for Australian energy commodities.