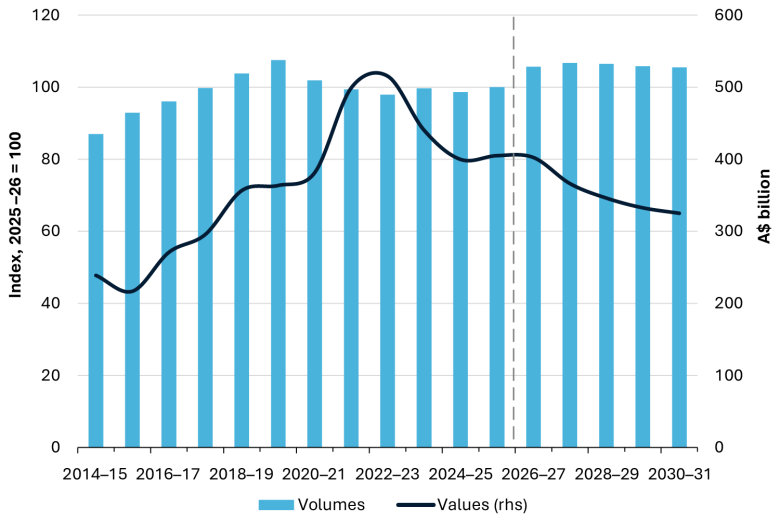

Compared to the December 2025 REQ, the outlook for Australian export earnings from resource and energy commodities in the next couple of years has strengthened. This boost is due to gains in the prices of energy commodities due to tensions and trade disruptions in the Middle East and the continued strong gold price. In the latter years of the 5-year outlook period, softening energy and bulk commodity prices will drive lower resource and energy commodity exports.

The June 2026 REQ forecasts resources and energy export earnings to rise from $385 billion in 2024–25 to $405 billion in 2025–26 and $416 billion in 2026–27. The forecasts represent upward revisions of $22 billion (2025–26) and $42 billion (2026–27) from the December 2025 REQ. Earnings are forecast to fall to $371 billion ($328 billion in real terms) in 2030–31 as commodity prices normalise.

Highlights from the June 2026 REQ:

- Exports in 2025–26 and 2026–27 have been revised up sharply. Higher-than-expected prices for energy commodities – due to Middle East supply disruptions – and for gold have driven the upgrade.

- Prices are expected to normalise over the outlook as market balances adjust. Energy commodity exports return to lower levels in the second part of the outlook, driven by lower thermal coal, LNG and oil export prices.

- Gold exports are estimated to have risen by 46% to $68 billion in 2025–26, driven by higher export volumes and a strong rise in prices. The gold price is forecast to average US$4,862 an ounce in 2026–27 and US$4,688 in 2027–28, with earnings peaking at $73 billion in 2026–27.

- Iron ore export earnings will continue to account for over 25% of all resource and energy commodity exports in the outlook period. With prices expected to soften of the back of rising global supply, exports are forecast to fall from $117 billion in 2025–26 to $80 billion in 2030–31.

- Demand for copper is being driven by increasing electrification and grid expansions. Rising prices and increasing export volumes are expected to lift copper exports from $13 billion in 2024–25 to $18.3 billion in 2030–31.

- Alumina prices have been affected by reduced demand from the Middle East although export volumes have been diverted to other destinations. Earnings are forecast to fall from over $12 billion in 2024–25 to $6.8 billion in 2025–26 before rebounding to $7.0 billion in 2030–31 in real terms. Aluminiumexports are forecast to be steady (at $6 billion in real terms) over the outlook period, with upside risk.

- Thermal coal export earnings are forecast to fall from $30 billion in 2025–26, to $25 billion in 2027–28 and $23 billion in 2030–31 in real terms.

- Metallurgical coal exports are forecast to fall from $38 billion in 2025–26 to $36 billion in 2027–28 and $34 billion in 2030–31 in real terms.

- LNG supply disruptions due to conflict in the Middle East are expected to keep prices elevated for a prolonged period, as damage to infrastructure will take time to repair. Export earnings are forecast to increase from $59 billion in 2025–26 to $65 billion in 2026–27, before declining to $41 billion in 2030–31 as Qatari and US LNG supplies build.

- Oil exports are projected to fall slightly in 2026–27 as falling volumes are offset by ongoing higher prices from the Middle East conflict. Oil exports are then forecast to fall to $5 billion in 2030–31 in real terms.

- Critical minerals export earnings are forecast to rise from around $17 billion in 2025–6 to $19 billion (in real terms) by 2030–31, driven largely by higher lithium exports. Australia’s lithium export earnings are forecast to increase from $9.9 billion in 2025–26 to $13 billion in 2026–27 (in real terms), before moderating to $10 billion in 2030–31. Lithium exports will account for more than half of total critical minerals earnings, with manganese, mineral sands and rare earths contributing most of the remaining revenue.