The September 2022 edition of the Resources and energy quarterly (REQ) was released today by the Department of Industry, Science and Resources.

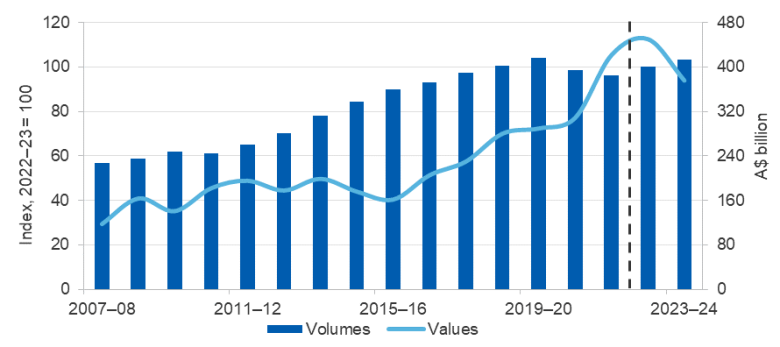

After a record $422 billion in 2021–22, resource and energy export earnings are forecast to reach $450 billion in 2022–23, before falling to $375 billion in 2023–24.

High energy prices and the strength of the US dollar against the Australian dollar are driving a surge in export earnings. Energy prices are elevated largely because of a looming drop in exports of gas, coal and oil from Russia, one of the world’s largest exporters of energy products. Despite falling export volumes, earnings from LNG are forecast to reach around $90 billion in 2022–23, and thermal and metallurgical coal are expected to earn around $120 billion in 2022–23.

Oil prices rose to their highest level in a decade in recent months, as the market reacts to looming sanctions on exports of Russian oil and related products by the EU. The oil price is likely to fall back over the outlook period, as an improvement in global supply gradually outpaces demand, affected by sluggish economic activity.

LNG spot prices remain extremely volatile amidst heightened global uncertainty. Spot LNG is expected to be relatively high for some time, whereas oil price–linked contract LNG prices are forecast to ease from high levels as oil prices settle back. Export volumes are forecast to fall from 83 million tonnes in 2021–22 to 80 million tonnes in 2022–23.

Australian metallurgical coal prices have declined, as steel markets weaken. Prices are expected to drift down but average relatively high levels over the next year, as sanctions curtail Russian coal exports. Australian thermal coal prices remain extremely high, as European nations look to build stockpiles ahead of the Northern Hemisphere winter. Prices are expected to ease over the outlook period, as trade flows reorganise and supply recovers.

The iron ore price has edged lower in recent months, as slowing global growth and weakness in China’s housing sector dampens iron ore demand. Iron ore prices are expected to ease further over the outlook period, as world supply gains faster than demand.

Australia is well placed in the push towards low emission technologies, with exports of metals used intensively in low emission technologies (copper, nickel and lithium) expected to generate around $33 billion in export earnings in 2022–23, double what they earned in 2020–21.

Lithium export earnings are forecast to increase by more than ten-fold in just two years from $1.1 billion in 2020–21 to almost $14 billion in 2022–23 before easing to around $13 billion in 2023–24. Surging prices are the primary driver, but export volumes are also expected to grow steadily as Australia maintains its position as the world’s largest lithium miner.

Base metal prices have stopped falling, helped by the prospect of stronger demand from China and the likely loss of some Russian supply (especially nickel and aluminium) from world markets. Prices should be flat to modestly weaker over the outlook period, as supply slowly catches up with demand and stockpiles build.

In volume terms, Australian resource exports are expected to show further growth over the outlook period. GDP and industrial production will grow modestly, increasing the demand for ferrous and non-ferrous metals.