About the Resources and Energy Quarterly

The Resources and Energy Quarterly contains the Office of the Chief Economist’s forecasts for the value, volume and price of Australia’s major resources and energy commodity exports. A ‘medium term’ (five year) outlook for Australia’s major resource and energy commodity exports is published in the March quarter edition of the Resources and Energy Quarterly. The June, September and December editions contain a ‘short term’ (two year) outlook.

Underpinning the forecasts contained in Resources and Energy Quarterly is the Office of the Chief Economist’s outlook for global commodity prices, demand and supply. The forecasts for Australia’s commodity exporters are reconciled with this global context. The global environment in which Australia’s producers compete can change rapidly. Each edition of Resources and Energy Quarterly factors in these changes, and makes appropriate alterations to the outlook, estimating the impact on Australian producers and the value of their exports.

Foreword

Australia’s resource and energy export earnings are forecast to reach $450 billion in 2022–23, surpassing last year’s record of $422 billion. Earnings are then forecast to fall to $375 billion in 2023–24 (still the third highest ever), as world supply responds to high prices amidst a soft demand backdrop.

Driving the current surge in resource and energy export earnings is a spike in energy prices and Australian dollar weakness against the US dollar. Energy prices are elevated largely because of a looming drop in exports of gas, coal and oil by Russia, one of the world’s largest energy exporters. Gas, LNG and thermal coal prices are at record levels, as Northern Hemisphere nations try to build stockpiles ahead of winter. Drought in large parts of Western Europe, the United States and southern China has exacerbated energy shortages. High energy prices have caused the curtailment of energy-intensive metal smelting/refining, especially in Western Europe. These output cuts have partly offset the impact of weaker metal demand (induced by a sharp rise in energy costs on consumers and slower global GDP growth).

Since the June 2022 Resources and Energy Quarterly, metallurgical coal prices have declined sharply, but the price of thermal coal and other energy commodities prices have remained extremely high. Bans on Russian exports of oil and other fossil fuels by most advanced Western countries are progressively taking effect. By early 2023, the market for Russian exports will have shrunk noticeably: transport and infrastructure constraints will likely prevent a full diversion of some of these energy commodities from the West to nations such as China and India. The net result is a drop in world energy supply, as some Russian output becomes stranded. We thus expect the prices of energy commodities to remain relatively high over the outlook period. High prices are likely to accelerate the medium/long term push towards the adoption of low emission technologies.

Despite weaker export volumes, earnings from LNG are forecast to be $90 billion in 2022–23, and thermal and metallurgical coal should both earn over $57 billion. This is two to three times higher than in 2020–21, when the COVID-19 pandemic saw energy prices dip sharply. Earnings from these commodities are likely to fall back towards pre-COVID-19 levels after 2023–24, as supply improves.

Australia is well placed in the global push towards low emission technologies: exports of metals used intensively in low emission technologies (namely copper, nickel and lithium) are expected to generate $33 billion in export earnings in 2022–23, more than double what they earned in 2020–21.

Since our last report, the Chinese Government has taken further action to support China’s economic growth. The economy has been impacted by COVID-19 lockdowns in some major cities, stresses in the property market and drought. The consensus amongst analysts is that China will not reach the government’s 2022 growth target of 5.5%. Further measures to boost growth may occur ahead of the Chinese Communist Party’s 20th National Congress in mid-October.

The IMF forecasts world GDP growth of 3.2% in 2022 and 2.9% in 2023, with China forecast to grow by 3.3% in 2022, rising to 4.6% in 2023. It is possible that inflation is peaking in most major economies; if inflation rates fall back towards target levels, monetary action may taper over 2023.

The La Niña weather pattern has returned, and this is likely to combine with a strongly negative Indian Ocean Dipole to result in wetter-than-normal conditions in eastern Australia over spring/summer. With Northern Hemisphere nations trying to build energy inventories, disruptions to Australian coal supply (due to possible flooding) will boost prices.

The risks to the forecast for Australia’s export earnings in 2022–23 and 2023–24 are skewed modestly to the downside. Markets appear to have priced in the loss of some Russian resource and energy commodity output from world supply. Should world supply hold up better than expected and/or demand prove weaker than expected, our exports could suffer. New outbreaks of vaccine-resistant COVID-19 strains also pose risks to the outlook. Especially so if they occur in China, where small outbreaks are currently being met with aggressive suppression measures.

Overview

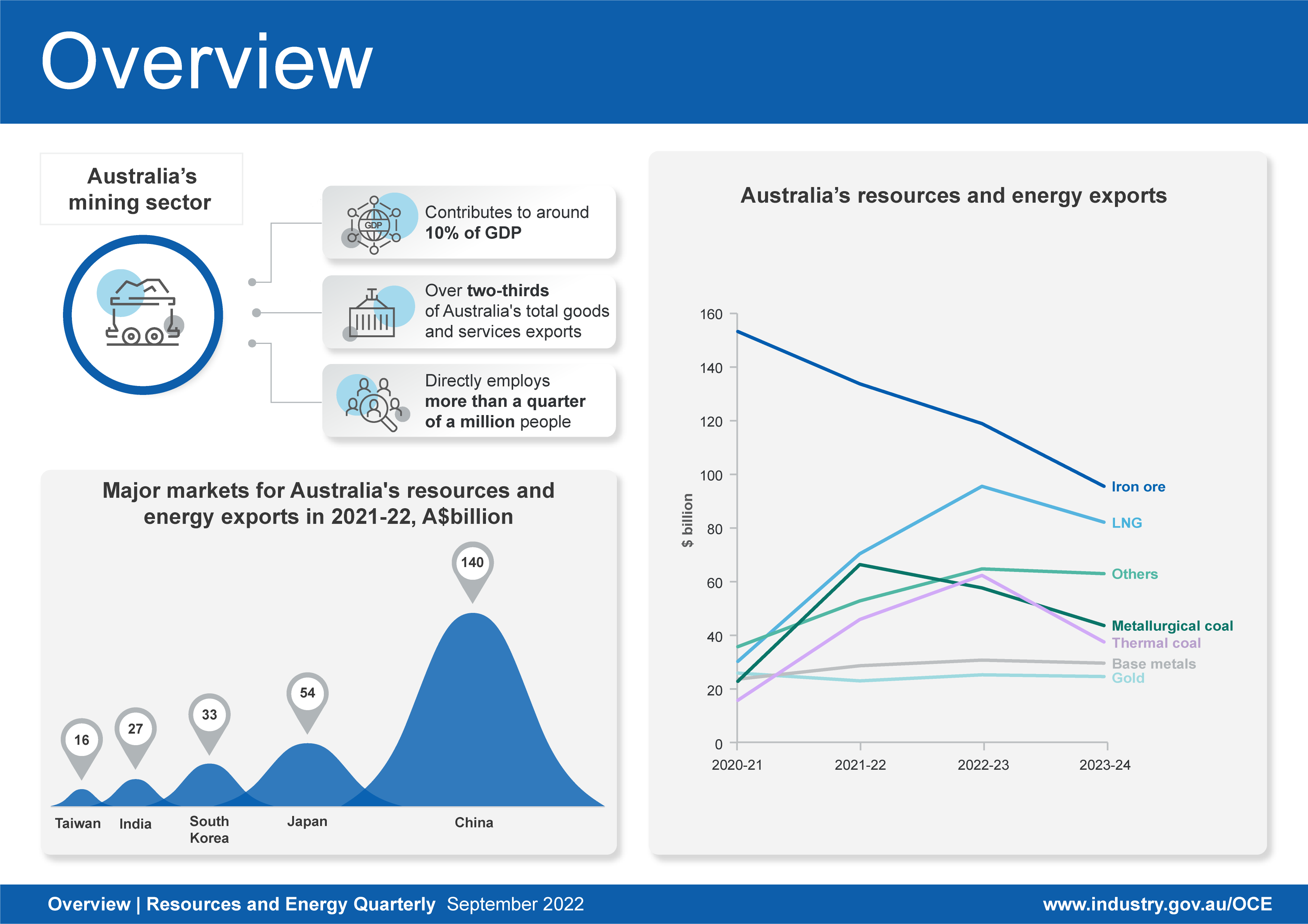

Australia’s resource and energy export earnings are forecast reach a new record of $450 billion in 2022–23

- Energy prices remain elevated, as the fallout from the Russian invasion of Ukraine exacerbates existing energy shortages. Energy prices (other than gas) will likely fall back in 2023 and 2024, as gains in world supply combine with soft demand.

- High energy prices and a weak Australian dollar against the US are driving a surge in export earnings. After a record $422 billion in 2021–22, resource and energy export earnings are expected to increase to $450 billion in 2022–23, before falling to $375 billion in 2023–24.

- Metals central to the global energy transition (copper, nickel, lithium) are set to earn $33 billion in 2022–23, double what they earned in 2020–21.

Macroeconomic outlook

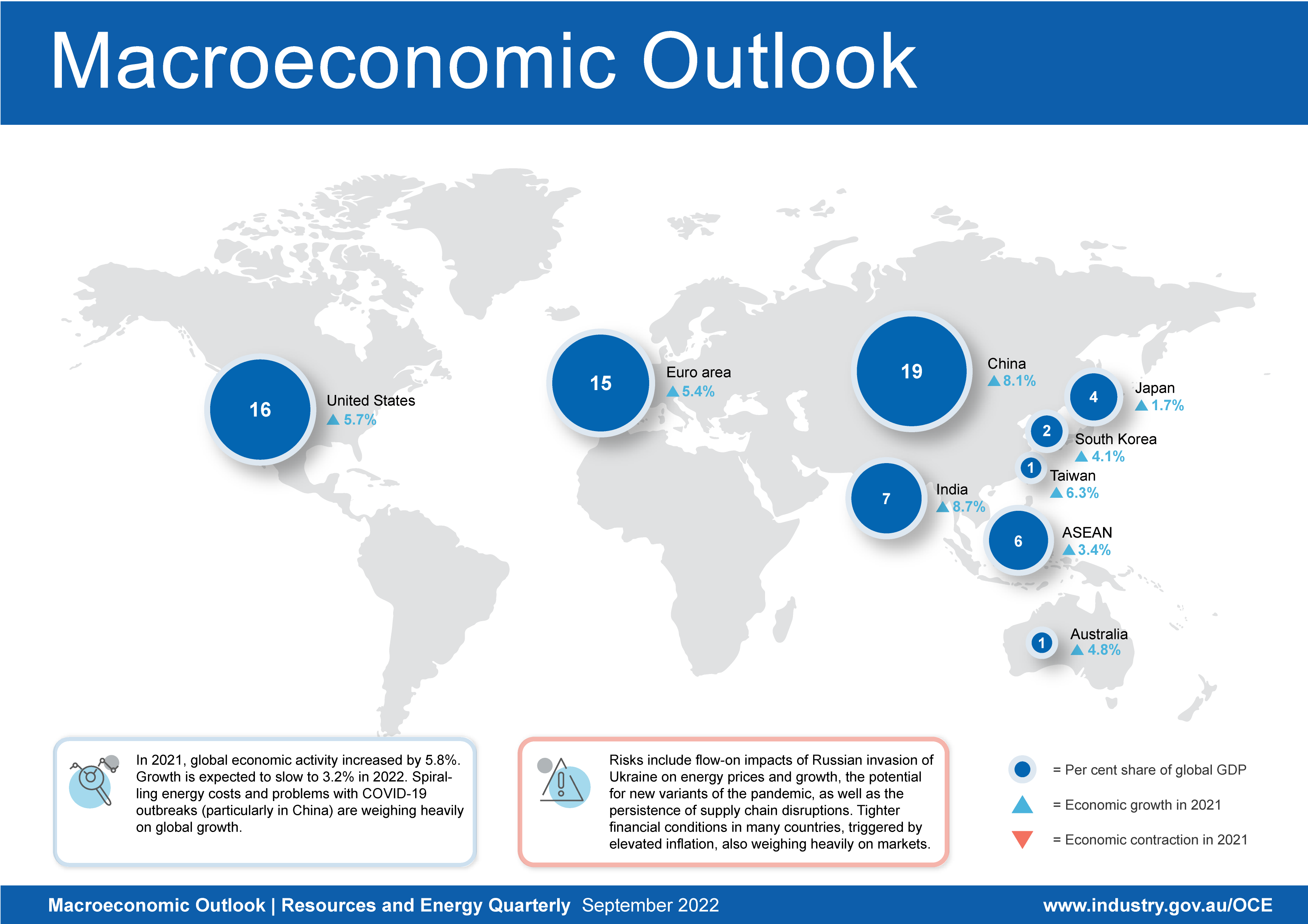

Global growth falls in the June quarter as the outlook darkens

- The global macroeconomic environment continues to weaken. Spiralling energy costs and problems with COVID-19 outbreaks (particularly in China) are weighing heavily on global growth.

- Tighter financial conditions in most major economies — triggered by elevated inflation — are heightening concerns about the global outlook.

- In July, the IMF forecast the world economy to grow by 3.2% in 2022 and 2.9% in 2023, around half the rate achieved in 2021 and a downward revision of 0.4 and 0.7 percentage points, respectively, since the previous forecast in April 2022.

Steel

Global steel production to fall in 2022 on faltering demand

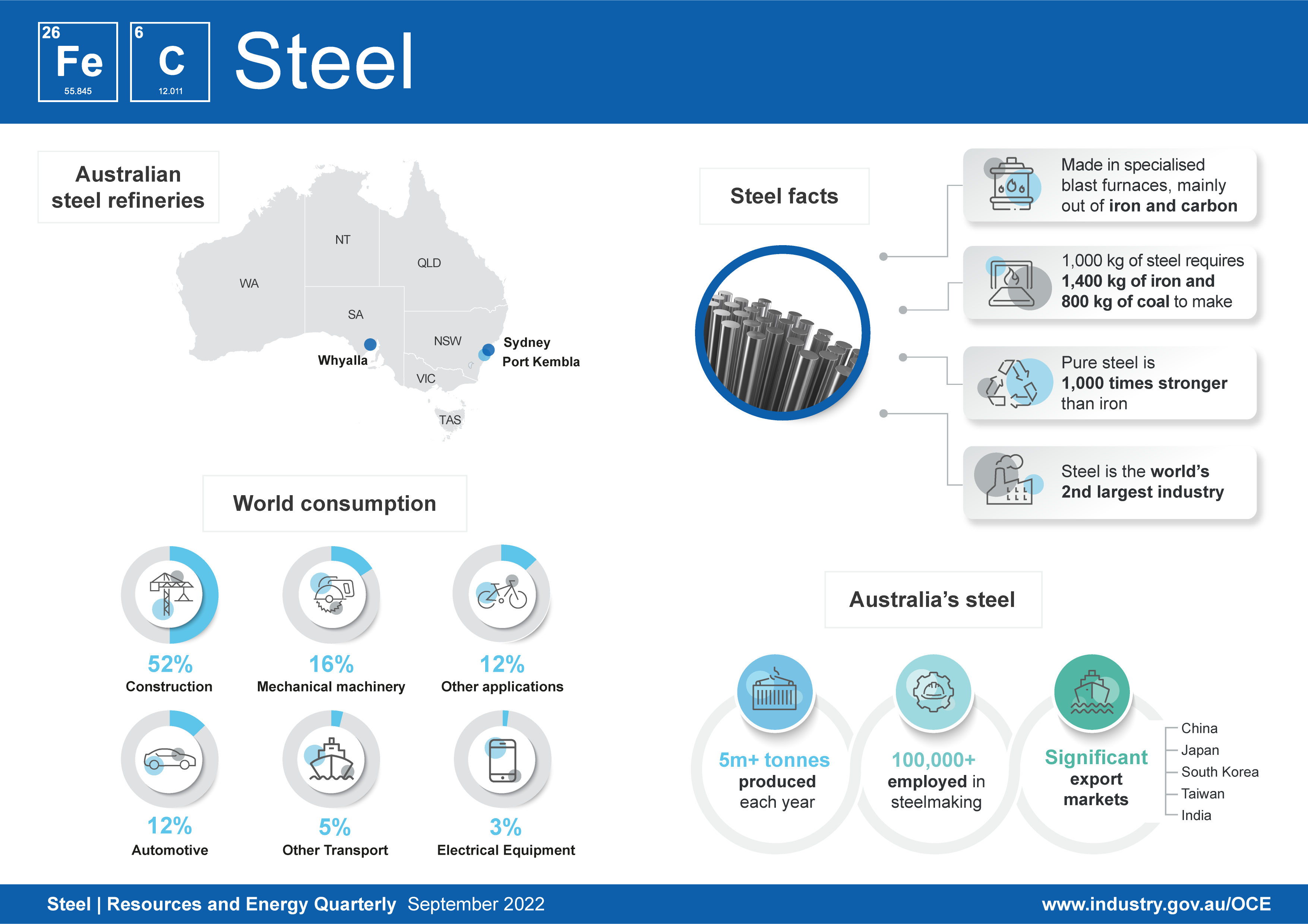

- World steel production fell 5.1% (year-on-year) in the first half of 2022. This followed new outbreaks of the COVID-19 pandemic in China, as well as ongoing weakness in its residential property sector. Energy shortages — intensified by the fallout from Russia’s invasion of Ukraine — are also weighing on activity in other major steel making nations.

- With growing signs of weak global economic growth, world steel production is forecast to fall 0.7% in 2022. This will be driven by current fragility in China’s residential construction sector, and global industrial production more broadly.

- Global steel output is expected to rebound to growth of 1.3% in 2023 and 1.1% in 2024, with large infrastructure rollouts planned or underway in a number of major economies. However risks remained skewed to the downside, with a more pronounced global slowdown or persistent energy shortages further threatening industrial production over the outlook.

Iron ore

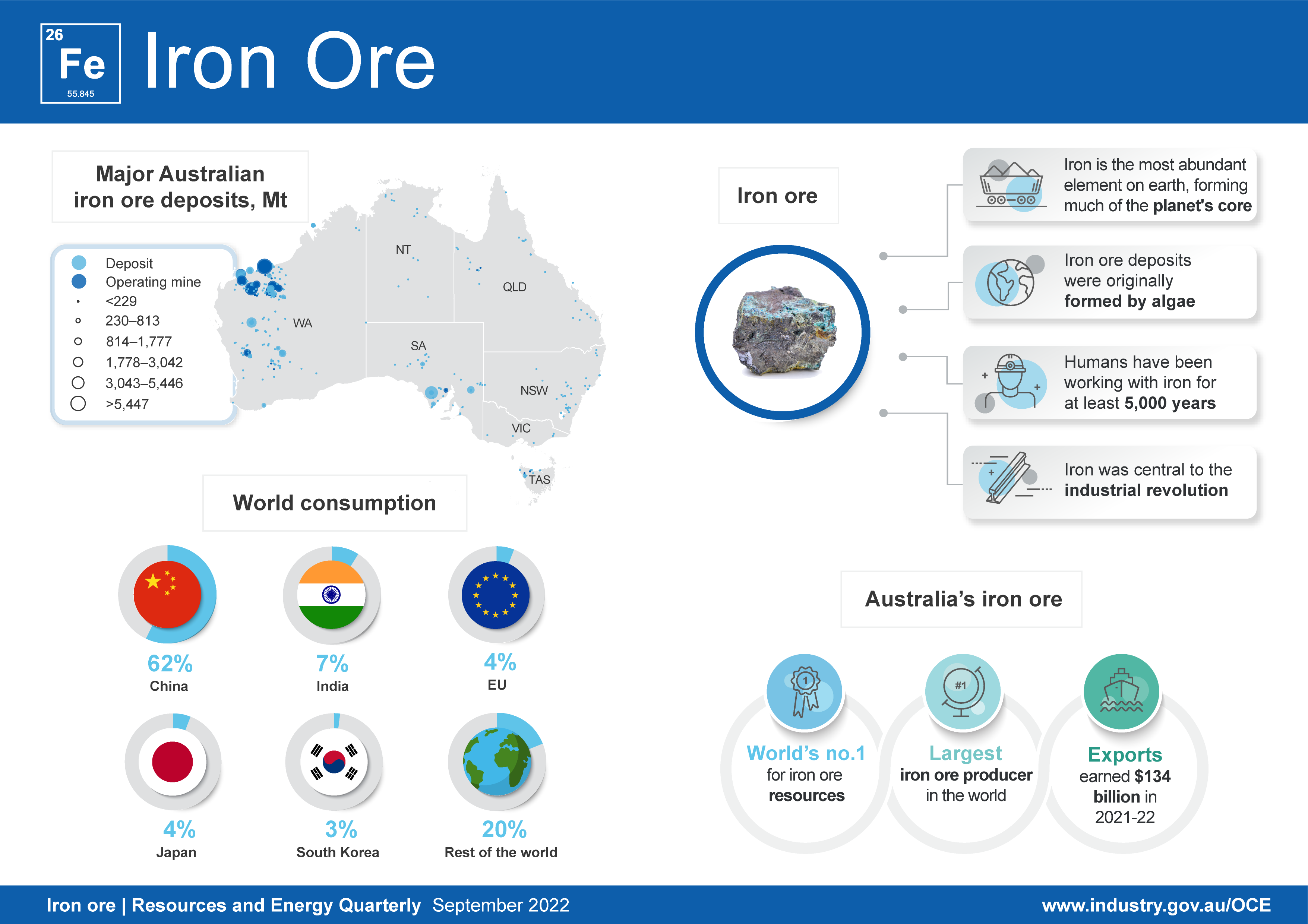

Iron ore prices dip in September quarter on weaker global steel demand

- Iron ore prices have fallen by around 20% in the September quarter 2022. Combined with growing global recessionary fears, new COVID-19 outbreaks and weakness in China’s housing sector, have dampened world steel and iron ore demand in recent months.

- Australian export volumes were 0.9% higher year-on-year in the first half of 2022, with new greenfield supply starting to come online from major producers. Exports are forecast to increase by 3.1% in 2022–23 to reach 903 million tonnes, and rise by 3.8% to 937 million tonnes in 2023–24.

- Lower prices over the outlook are expected to see Australia's iron ore export earnings ease from $134 billion in 2021–22 to $119 billion in 2022–23, and then to $95 billion in 2023–24.

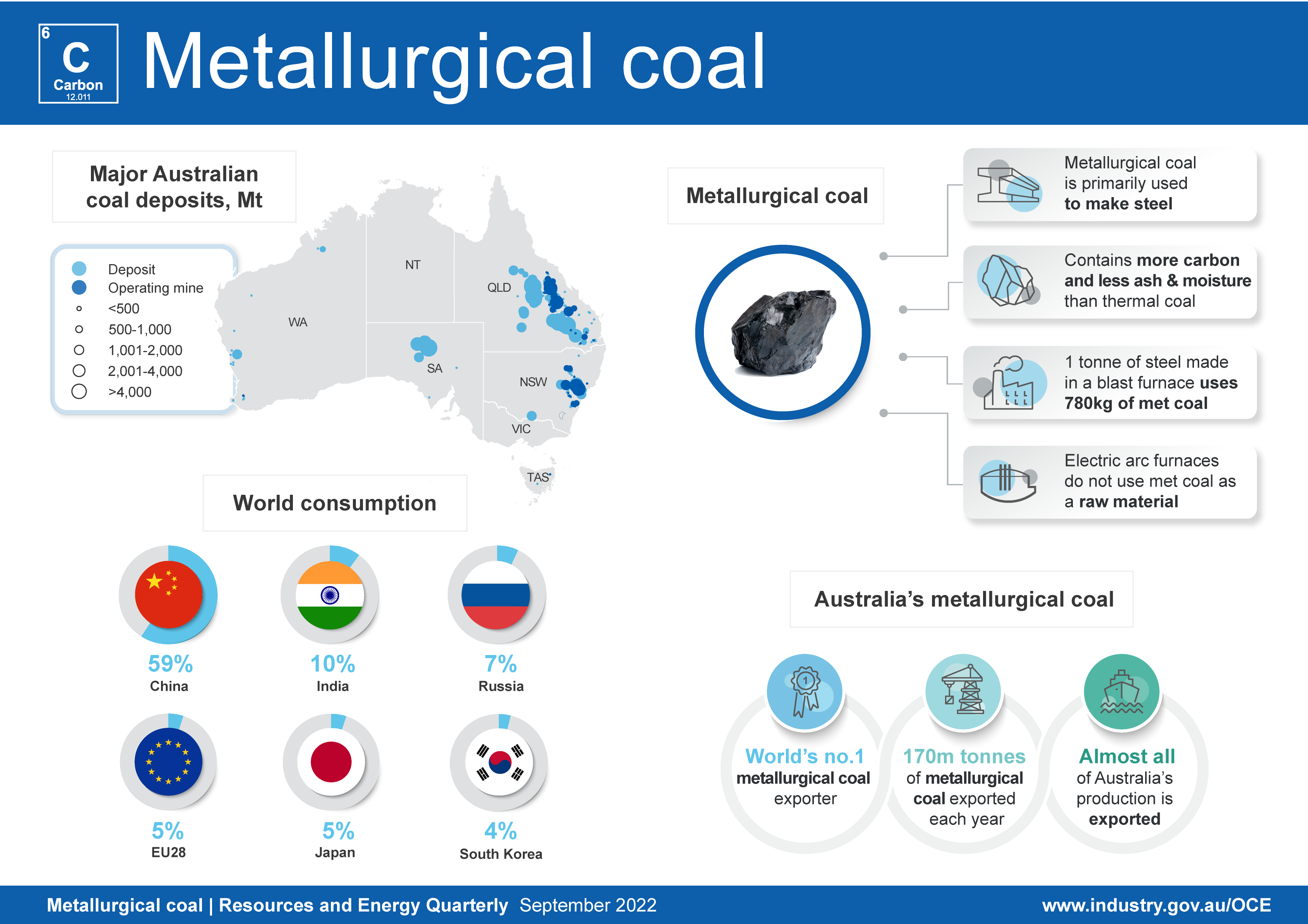

Metallurgical coal

Metallurgical coal export earnings have retreated following a strong rise earlier in the year

- Metallurgical coal prices have eased back from historic highs in the September quarter. The Australian premium hard coking coal price is forecast to average almost US$400 a tonne in 2022, but is expected to fall by almost half as supply conditions normalise, ultimately reaching around US$220 a tonne by 2024.

- Higher production in NSW and Queensland is expected to push up Australia’s exports, from 171 million tonnes in 2020–21 to 180 million tonnes by 2023–24.

- Australia’s metallurgical coal export values are forecast to track with price movements, rebounding from $23 billion in 2020–21 to peak above $60 billion in 2021–22, before falling back to $43 billion in 2023–24.

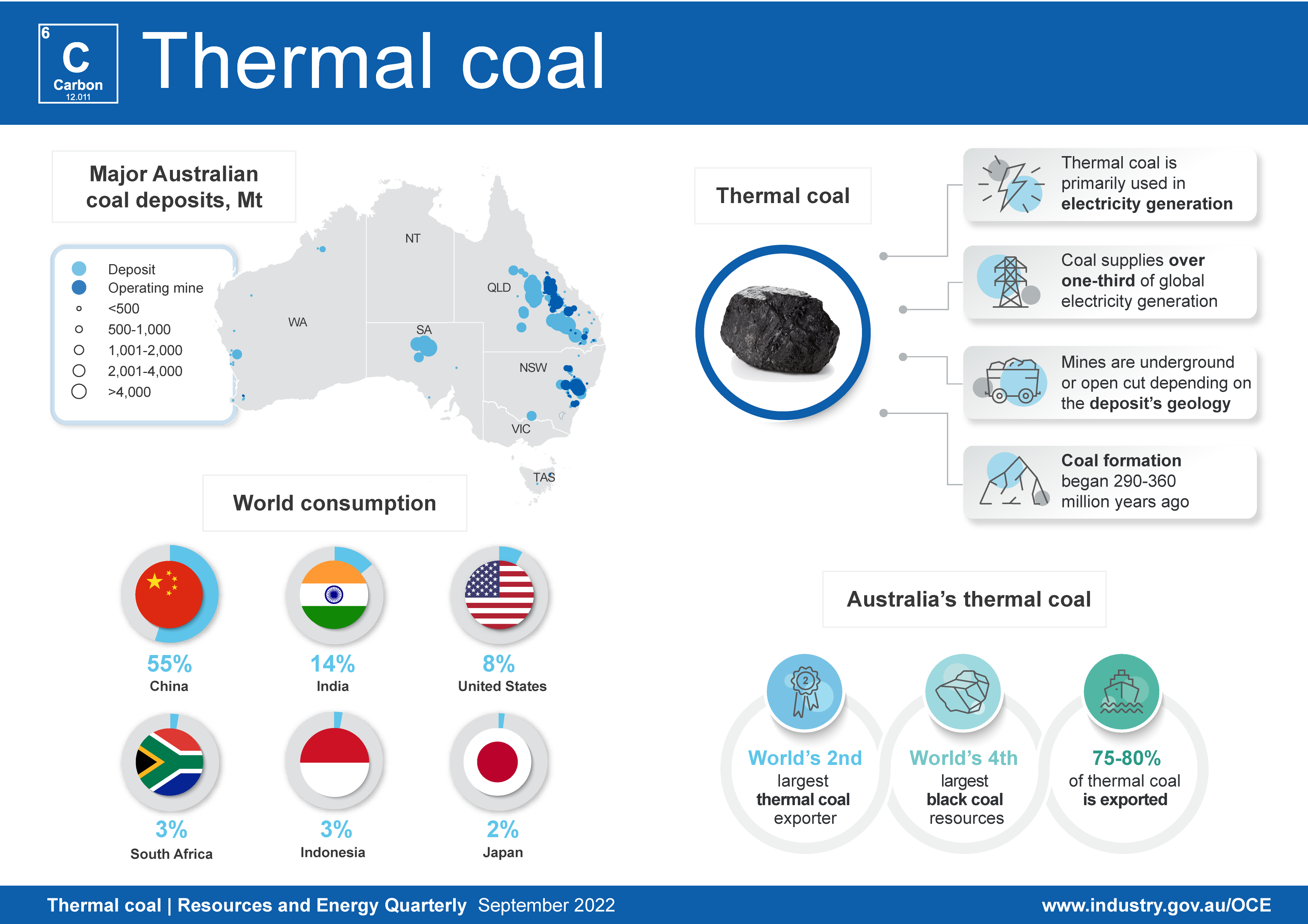

Thermal coal

Australia’s thermal coal export earnings have remained historically high amidst ongoing global supply issues

- Thermal coal prices remain extremely high, driven by weather and COVID-19 disruptions, as well as market uncertainties linked to the Russian invasion of Ukraine. As more normal conditions return, the Newcastle benchmark price is forecast to ease from an average of US$333 a tonne in 2022, to around US$125 in 2024 (still well above historical averages).

- A resolution of recent supply disruptions is expected to see Australian thermal coal exports increase from 192 million tonnes in 2020–21 to 203 million tonnes by the end of the forecast period.

- Record prices are expected to see export values reach $62 billion in 2022–23 before a (price-driven) easing to about $38 billion in 2023–24.

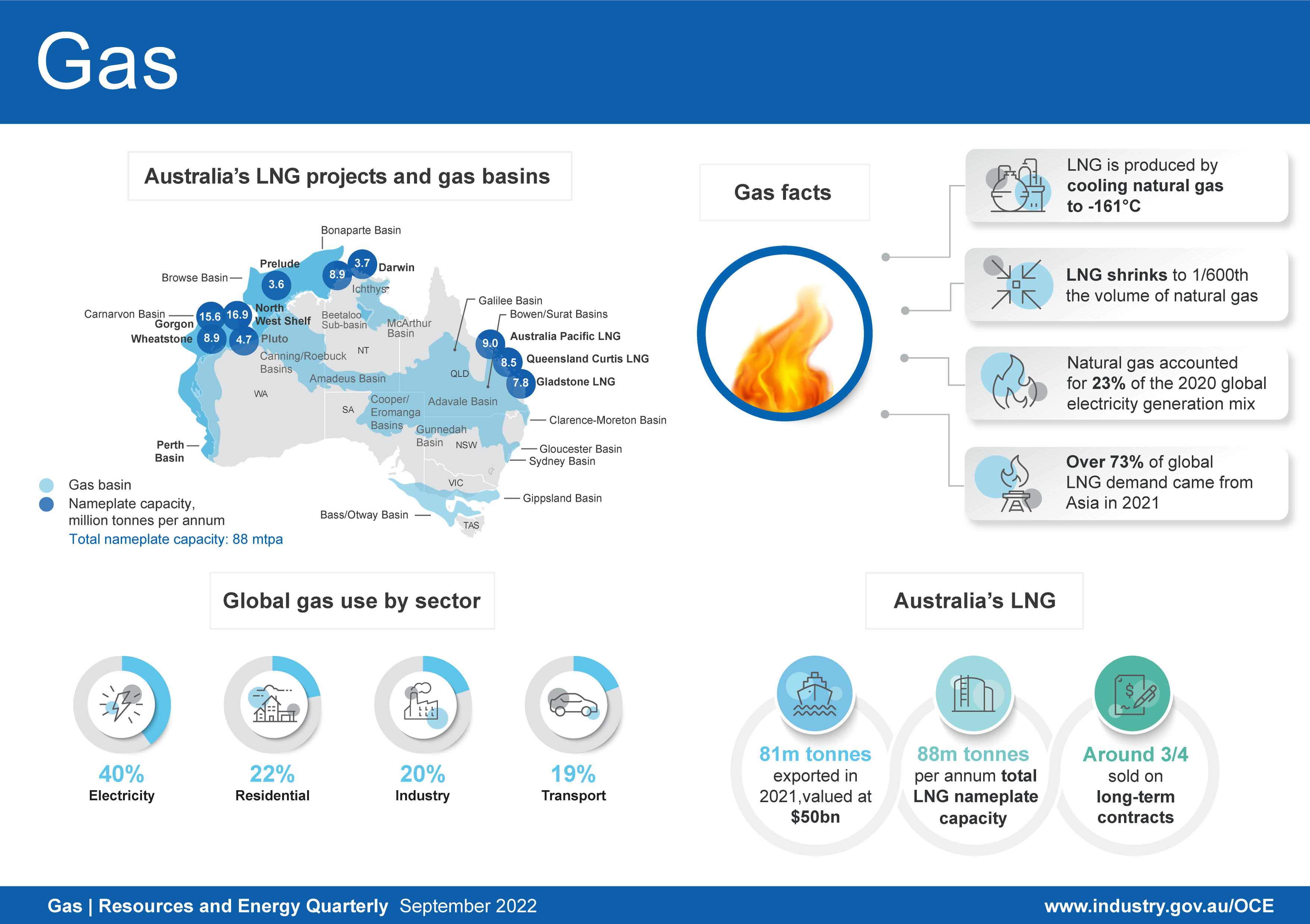

Gas

Australia’s LNG export earnings to rebound strongly in 2021–22, as prices recover

- Asian LNG spot prices and oil-linked contract prices are expected to remain high over the two-year outlook.

- Australian export volumes reached 83 million tonnes in 2021–22, as higher capacity utilisation rates offset technical issues at other plants. Volumes should then fluctuate between 79 and 81 million tonnes over the outlook.

- Australia’s LNG export earnings doubled from $30 billion in 2020–21 to $70 billion in 2021–22. They are forecast to reach $90 billion in 2022–23, as oil-linked contract prices and Asian LNG spot prices remain elevated. Export earnings are forecast to return to around $81 billion by the end of the outlook period.

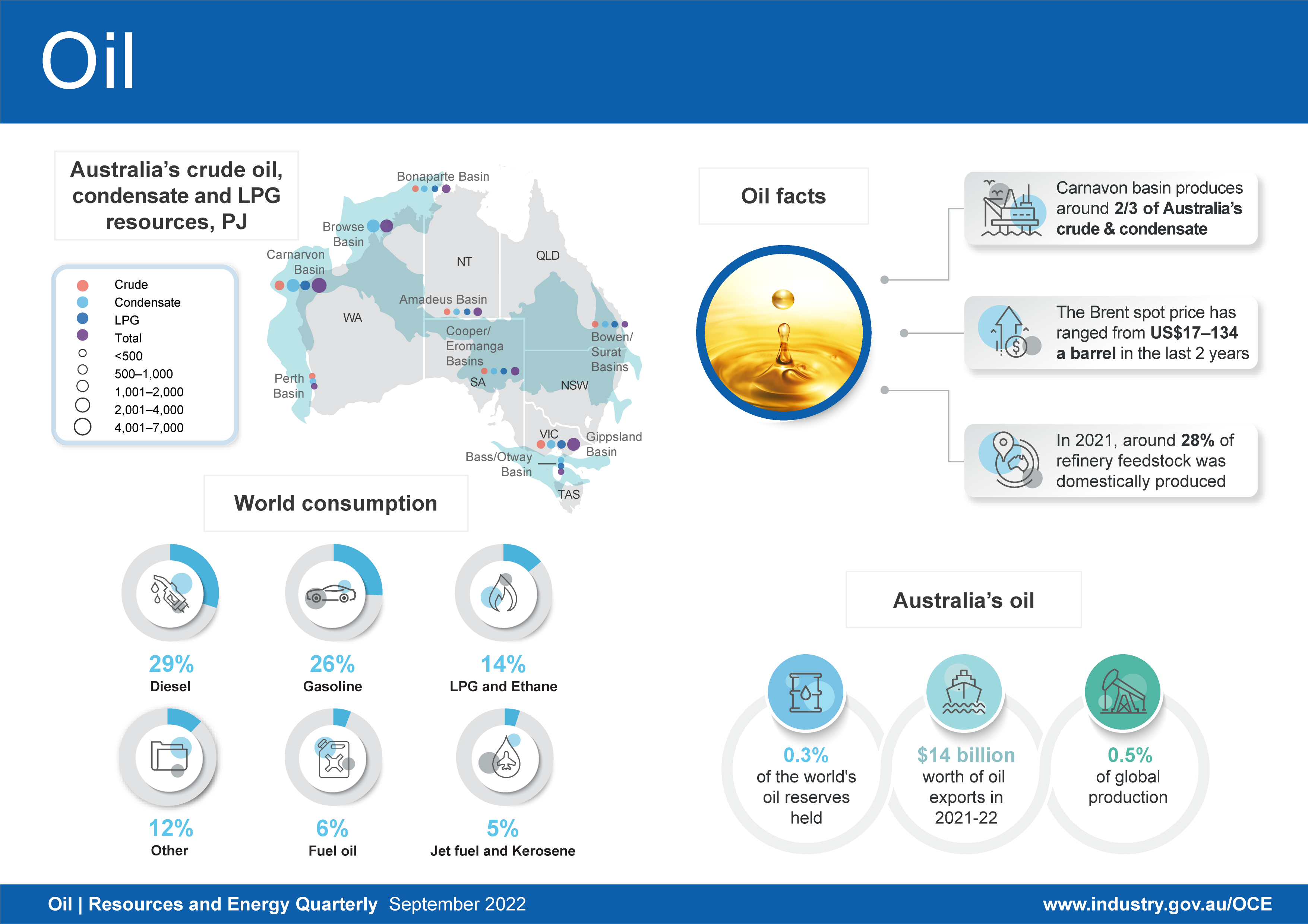

Oil

Australian crude and condensate export earnings lifting significantly with higher prices

- Oil prices are forecast to follow a downward trend, following multi-year highs in the first half of the year. However, the fallout of Russia’s invasion of Ukraine and global economic developments are driving elevated levels of uncertainty for forecasts. Brent crude oil is forecast to average US$103 a barrel in 2022, before declining over the rest of the forecast period.

- Australian crude oil and feedstock exports rose to 292,000 barrels a day in 2021-22. Export volumes are forecast to decrease to 267,000 barrels a day in 2022-23, before returning to 286,000 barrels a day in 2023-24.

- Australian oil export earnings increased by a staggering 88% to $14.0 billion in 2021–22, due to the strong surge in oil prices. Sustained elevated prices should result in earnings reaching $15 billion in 2022–23. Earnings for 2023-24 are forecast to return to $13.4 billion, as prices fall from current highs

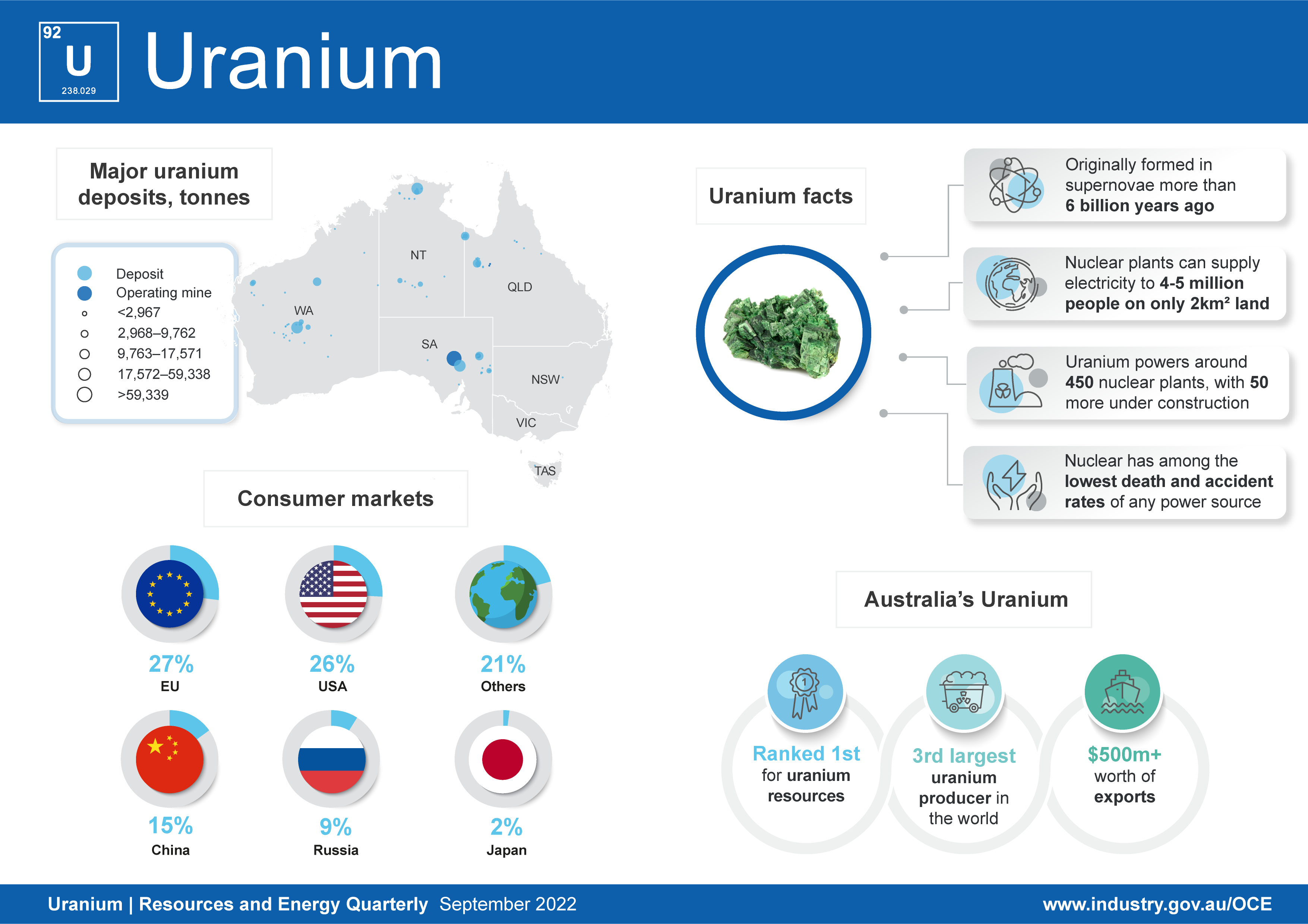

Uranium

Uranium prices are rising, with volumes also set to grow.

- Uranium prices are forecast to lift from US$51 a pound in 2022 to US$60 a pound by 2024. Uranium shortfalls have become a prospect in the wake of years of low prices and underinvestment.

- Australian exports are forecast to decline to 4,500 tonnes in 2021–22. This is expected to rise to around 5,500 tonnes by 2023–24 as the Honeymoon mine reopens.

- Price and volume growth is expected to increase uranium export values from $564 million in 2021–22 to around $880 million by 2023–24.

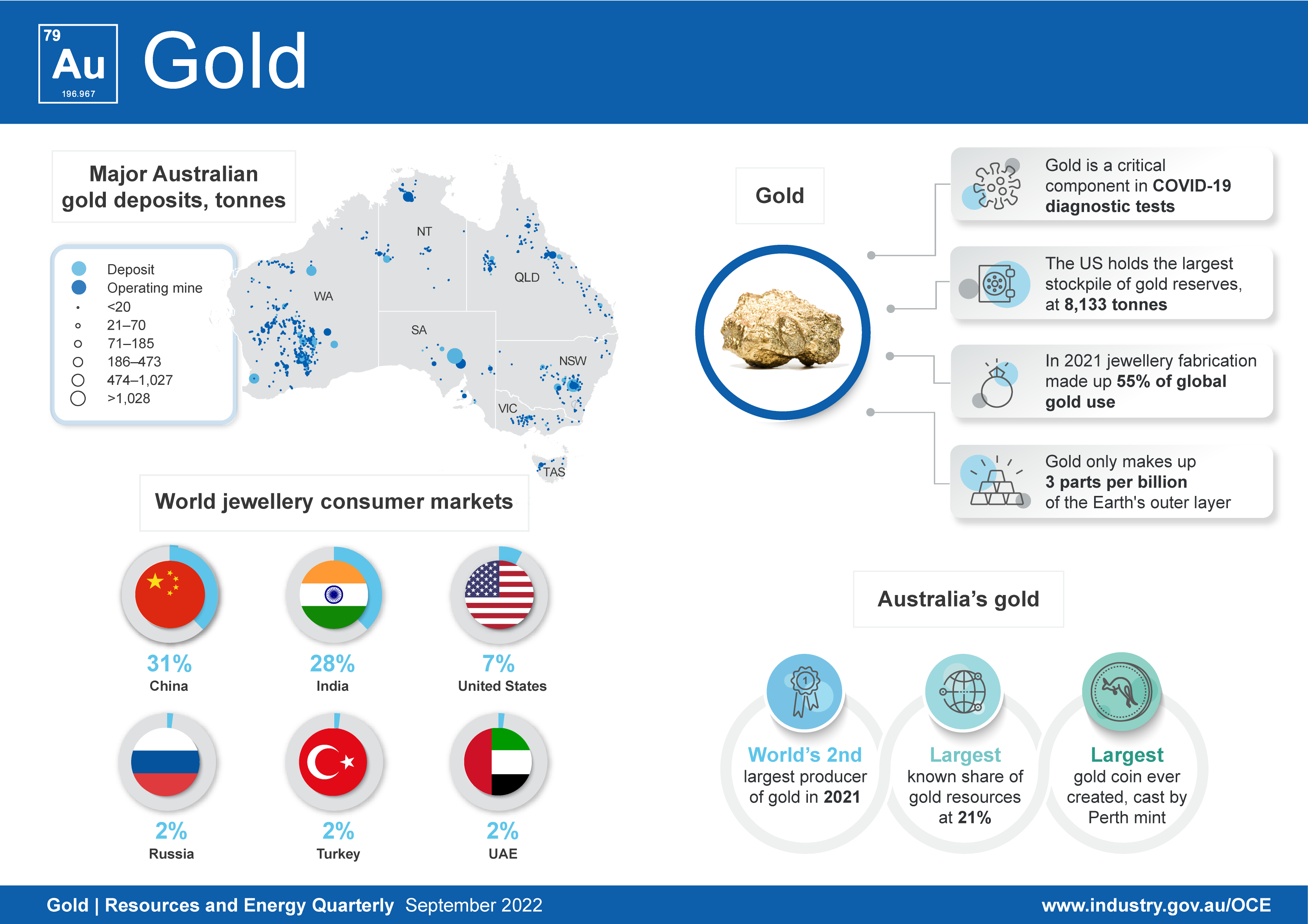

Gold

Australia’s gold export earnings forecast to increase to almost $26 billion in 2022–23.

- Gold prices are expected to average about US$1,788 an ounce in 2022, before falling to an average of US$1,614 in 2024 as monetary policy continues to tighten in advanced economies, and safe-haven demand eases.

- Australian gold mine production in the June quarter 2022 was 0.9% higher year-on-year at 81 tonnes. Labour and skill shortages were still affecting mining operations, however production was 10% higher than the disrupted March quarter 2022. Australian production is forecast to rise from 308 tonnes in 2021–22 to 349 tonnes in 2023–24 as new projects and expansions of existing projects come online.

- Gold earnings are forecast to rise from $23 billion in 2021–22 to about $25 billion in 2023–24, as rising gold export volumes exceed the forecast decline in gold prices.

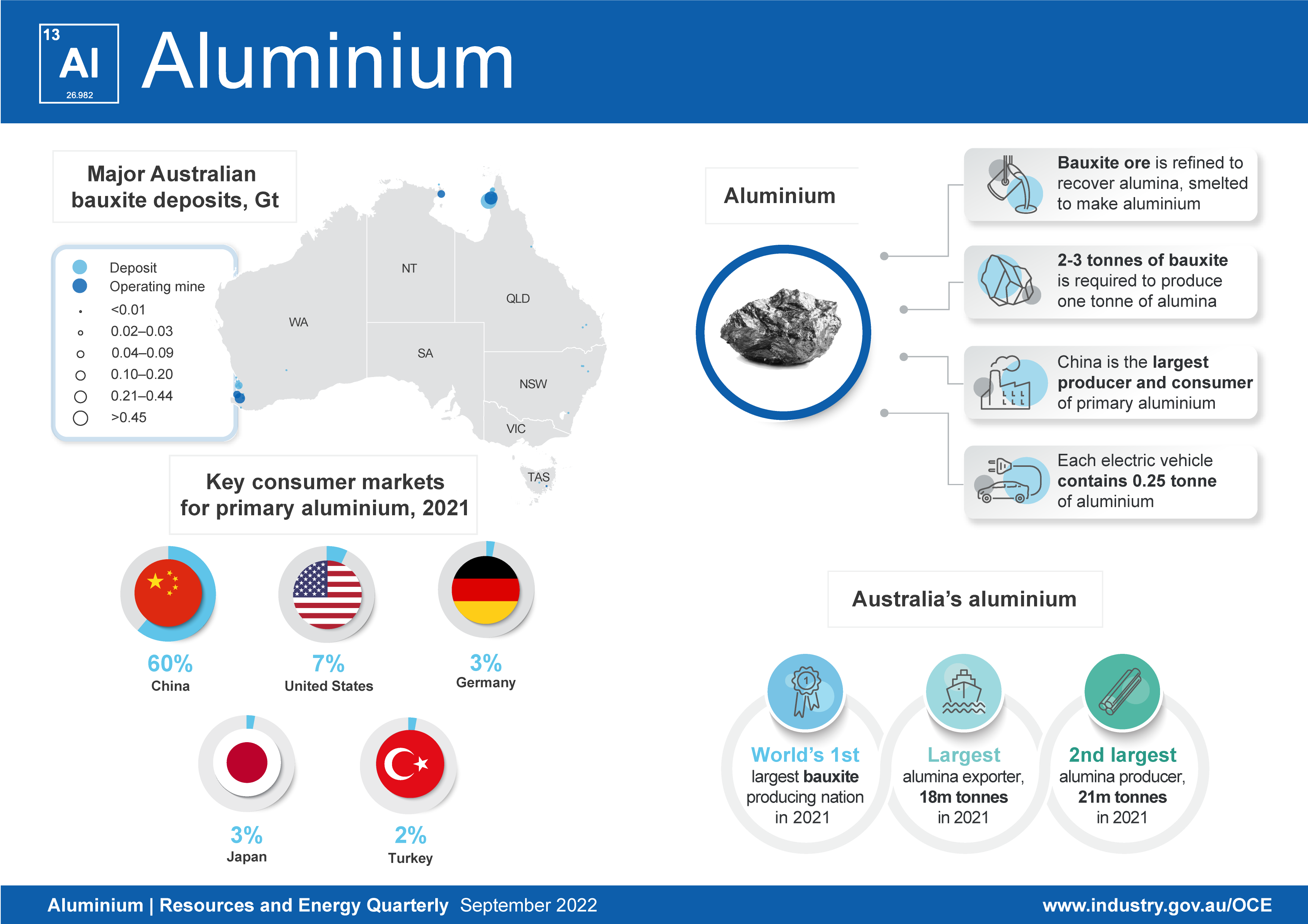

Aluminium, alumina and bauxite

Australia’s aluminium, alumina and bauxite export earnings to be steady at $15 billion in 2022–23

- Lower primary aluminium supply from China and Europe is expected to keep aluminium prices at high levels in 2022, averaging US$2,790 a tonne. Prices are forecast to drift down through the rest of the forecast period, averaging US$2,490 a tonne in 2024, getting some support from growing demand for new, energy-efficient cars and technologies.

- Australia’s annual primary aluminium and alumina output is expected to be broadly steady over the outlook period: at around 1.6 million tonnes of primary aluminium and 21 million tonnes of alumina. Australia’s annual bauxite output is expected to increase from 106 million tonnes in 2022–23 to nearly 109 million tonnes in 2023–24.

- Australia’s aluminium, alumina and bauxite export earnings are forecast to be steady at $15 billion a year in 2022–23 and 2023–24.

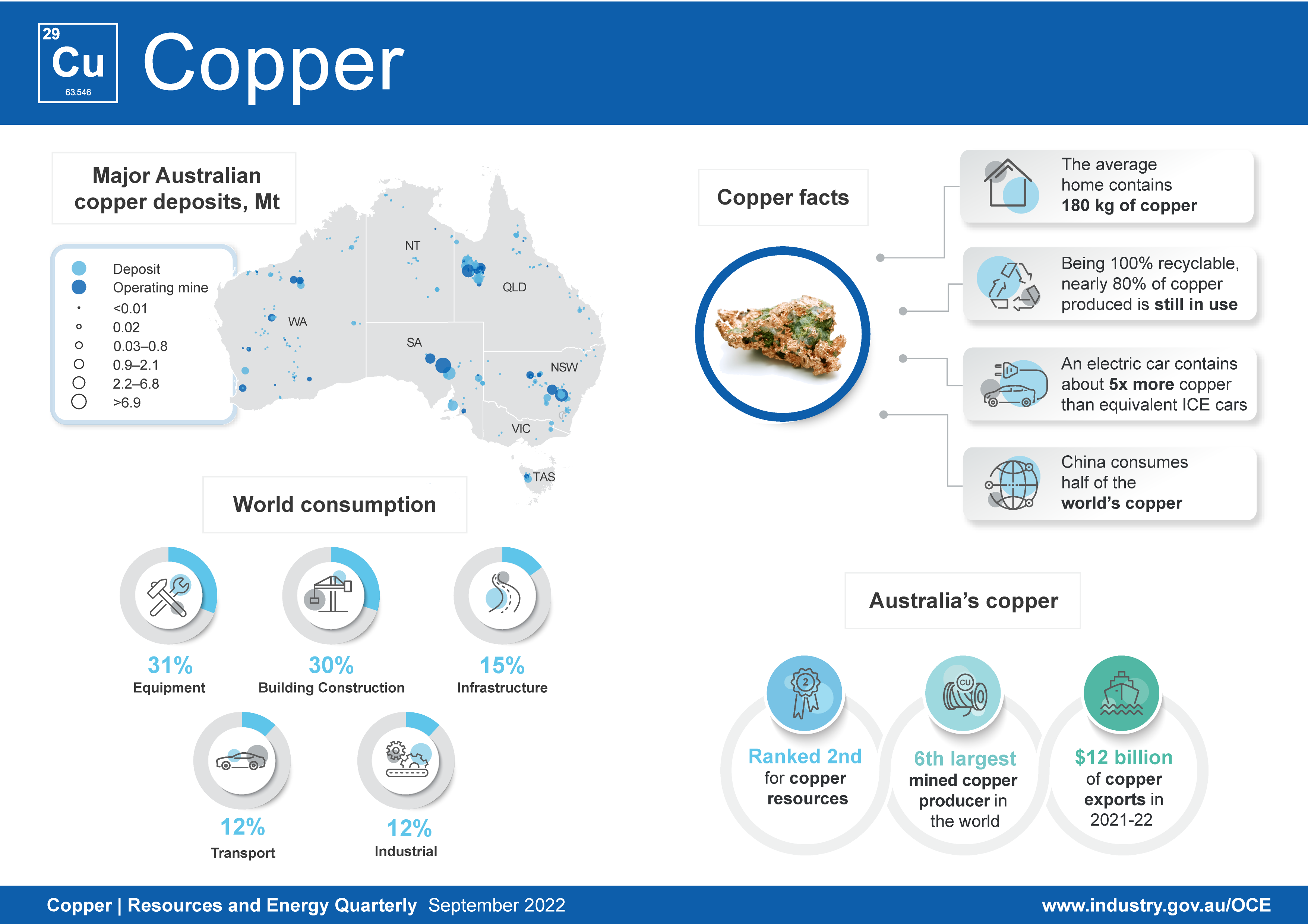

Copper

Copper export earnings to grow as production ramps up

- Copper prices are forecast to fall 4.9% to below US$8,900 in 2022, as COVID-19 containment measures and high energy prices weigh on demand. Prices are forecast to fall to US$8,300 a tonne in 2024 as mine production grows.

- Australia’s copper exports fell to 802,000 tonnes in 2021–22 as scheduled maintenance reduced production. Copper exports are expected to grow to 977,000 tonnes by 2023–24 as production from new mines and mine expansions come online.

- As output and export volumes grow, Australia’s copper export earnings are projected to lift from $12.3 billion in 2021–22 to $13.9 billion in 2023–24.

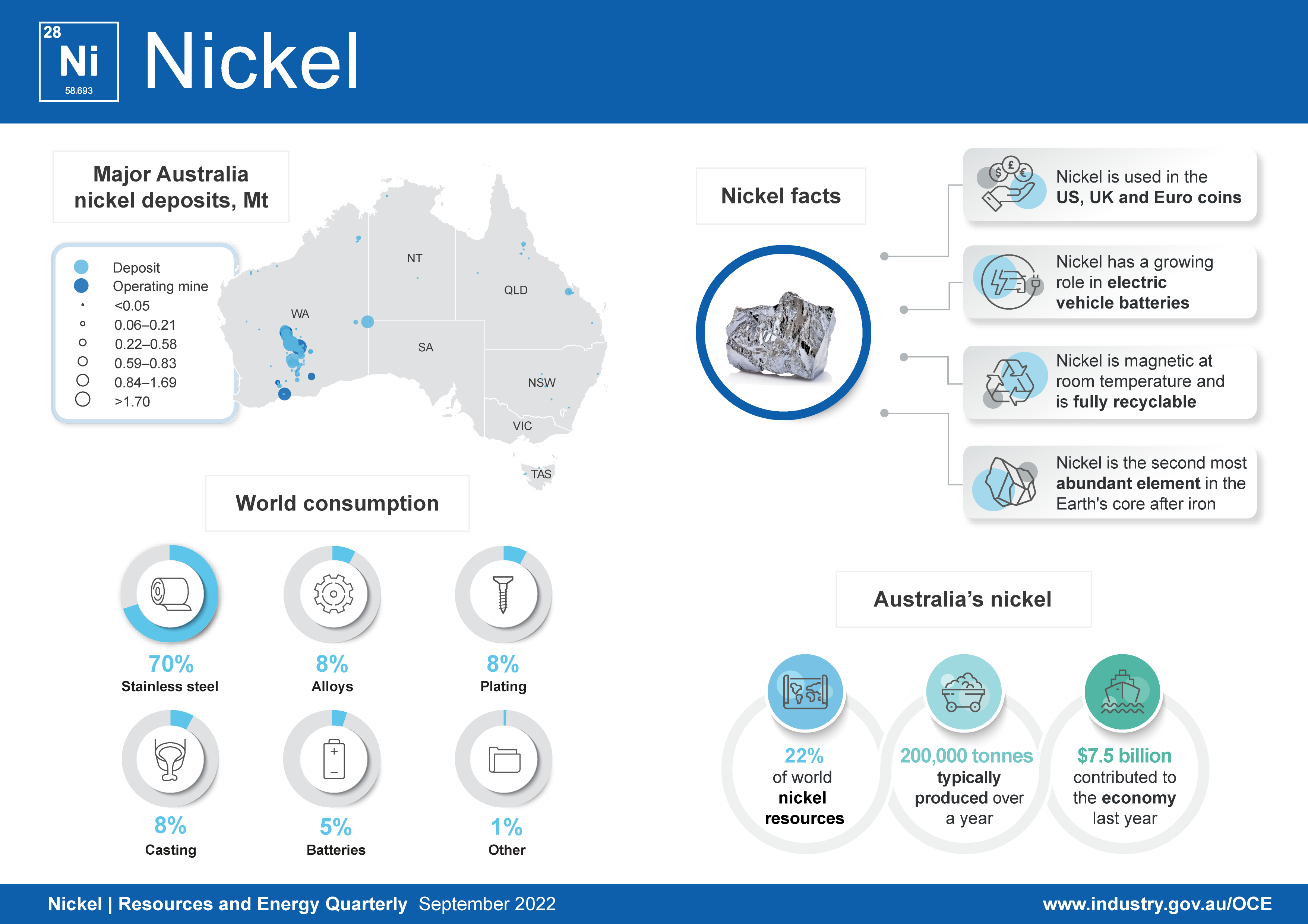

Nickel

Increased production to boost export volumes and earnings

- Nickel prices are expected to average US$24,900 a tonne in 2022, boosted by the fallout from the Russian invasion of Ukraine. Prices are expected to ease over the outlook period, as a result of increased Indonesian production and improving liquidity in the LME nickel market.

- Recent high prices have boosted Australia’s nickel export earnings, which reached $4.4 billion in 2021–22. Export earnings are forecast to rise to $5.1 billion in 2022–23, before easing to $4.6 billion in 2023–24.

- Australia’s export volumes are estimated to rise from 157,000 tonnes in 2021–22 to 202,000 tonnes in 2023–24, supported by the need for Australian nickel for the transition to low-emissions technologies.

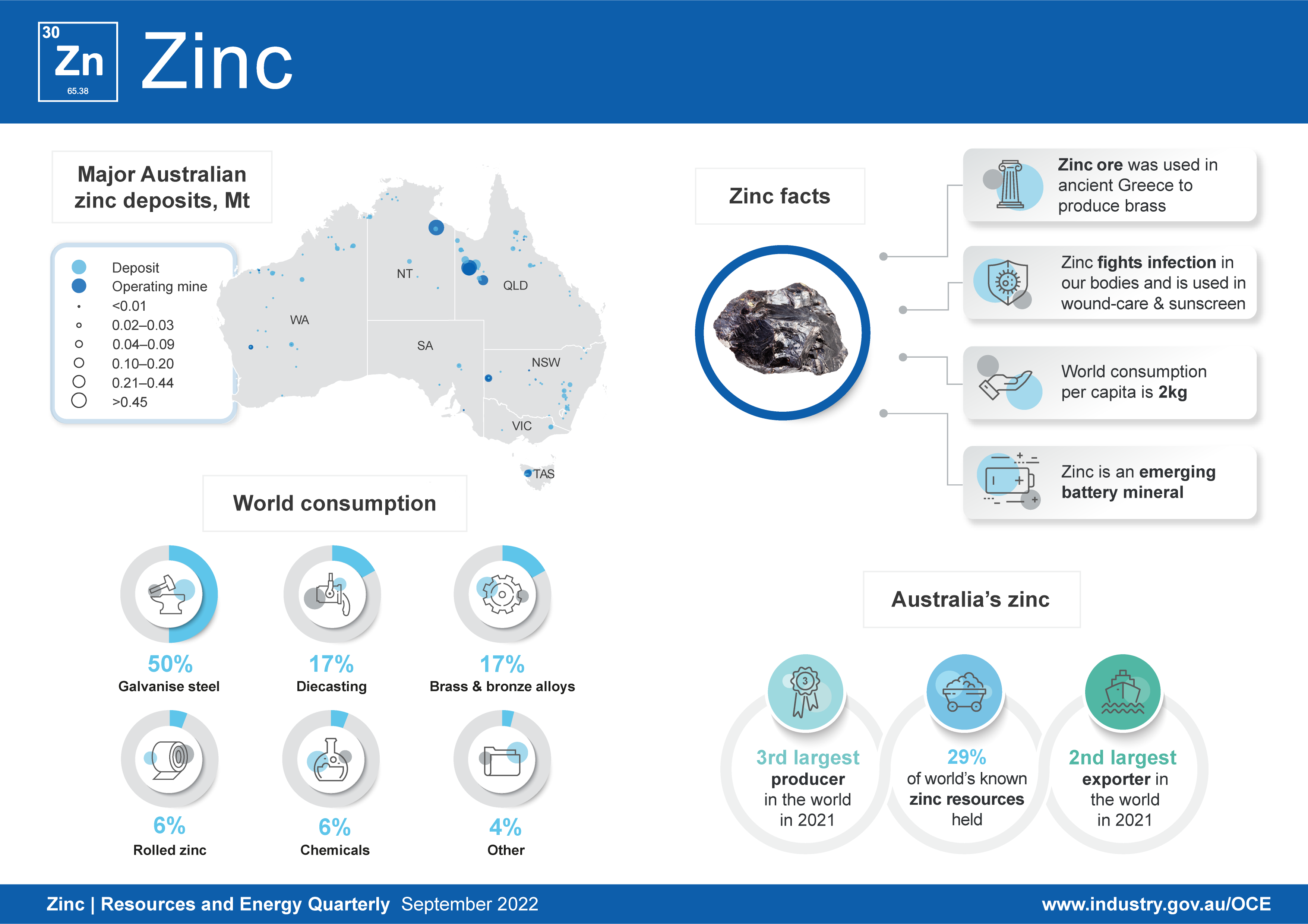

Zinc

High prices to drive export earnings over the outlook period

- The LME zinc spot price is forecast to average around US$3,600 a tonne in 2022, with supply pressured by reduced production of refined zinc in Europe. Prices are forecast to ease over the outlook to around US$3,000 a tonne by 2024, as supply pressure ease.

- Encouraged by high prices, Australia’s zinc production is forecast to rise by 5.0% per year to around 1.4 million tonnes by 2023–24.

- Australia’s zinc export earnings are forecast to peak at $5.3 billion in 2022–23, before easing in 2023–24 to $4.7 billion.

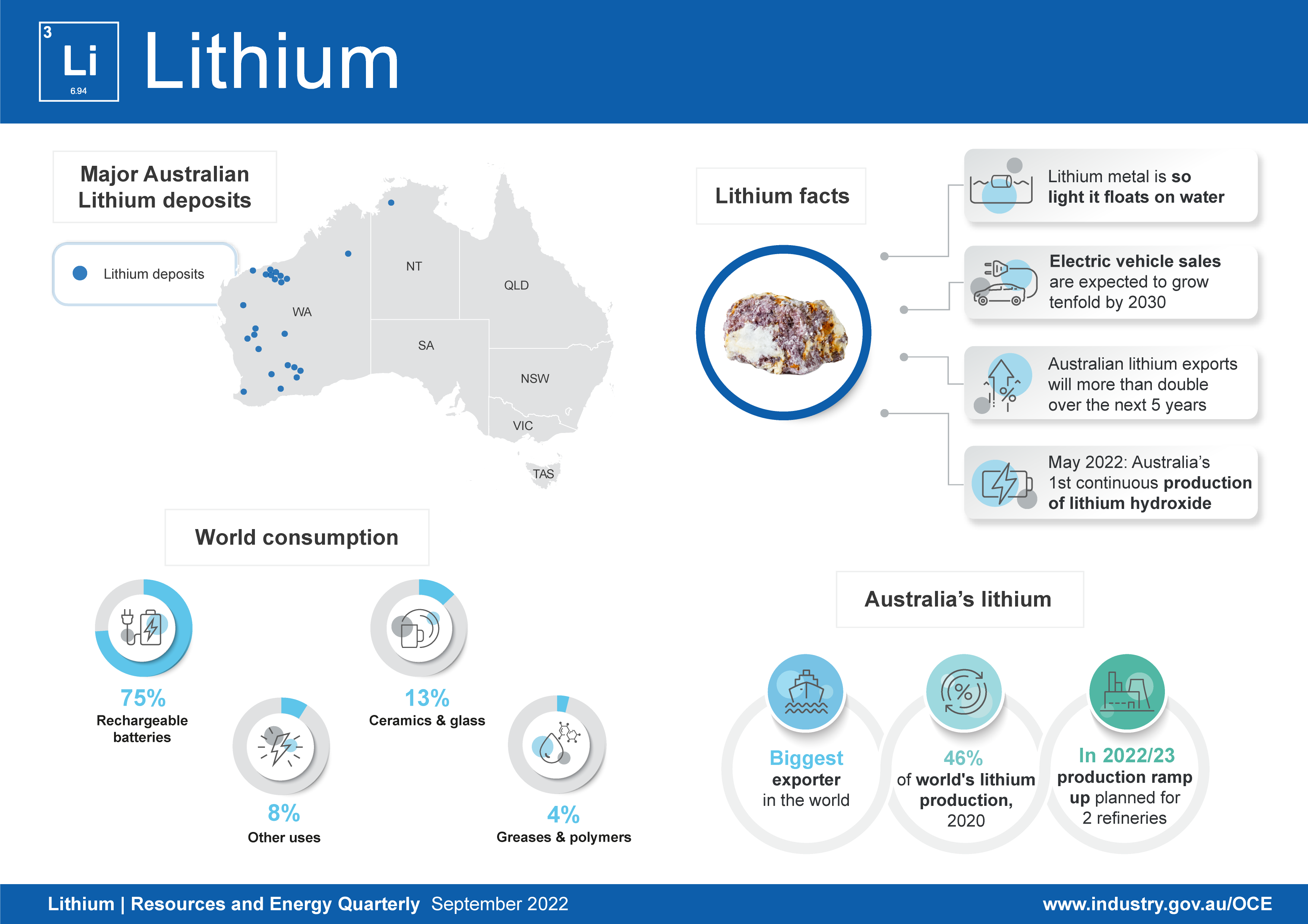

Lithium

Lithium set to become a $10 billion-plus export industry within a year

- Spodumene prices are forecast to rise from an average US$598 a tonne in 2021 to US$2,730 a tonne in 2022, and US$3,280 a tonne in 2023 before moderating to US$2,490 in 2024. We expect lithium hydroxide prices to lift from US$17,370 a tonne in 2021 to US$38,575 a tonne in 2022 and US$51,510 in 2023, and moderate to US$37,650 by 2024.

- Australia’s lithium production is forecast to grow from 247,000 tonnes of lithium carbonate equivalent (LCE) in 2020–21 to 387,000 tonnes in 2022–23 and 469,000 tonnes of LCE in 2023–24.

- Australia’s lithium export earnings are forecast to increase by more than ten-fold in just two years from $1.1 billion in 2020–21 to $13.8 billion in 2022–23, and ease to $12.9 billion by 2023–24.